In its consultation on accelerating home building, the Scottish Government rightly identifies that “we urgently need to see more homes built, at a faster pace, now and in the years ahead”

. This is part of its “Housing Emergency Action Plan” and to address the challenges of dwindling housebuilding starts and serving 250,000 individuals on housing waiting lists

. Housebuilding has dropped from a recent high of 25,000 starts in 2019 to 16,000 in 2024.

While the consultation focuses on issues with housing delivery, the 2020s has also seen a decline in residential permissions themselves. In the absence of a significant uptick in the number of homes being permitted, the issue of delivery is likely to get significantly worse. This Insight focuses on the conditions contributing to the recent decline in planning consents, and particularly the role of recent changes in worsening the conditions for housebuilding.

When it was adopted in February 2023, NPF4—prepared and adopted by the Scottish Government—became part of the development plan. Unlike its predecessors, its policies became a consideration in every planning decision made by a local planning authority (LPA), alongside their own Local Development Plan (LDP) policies.

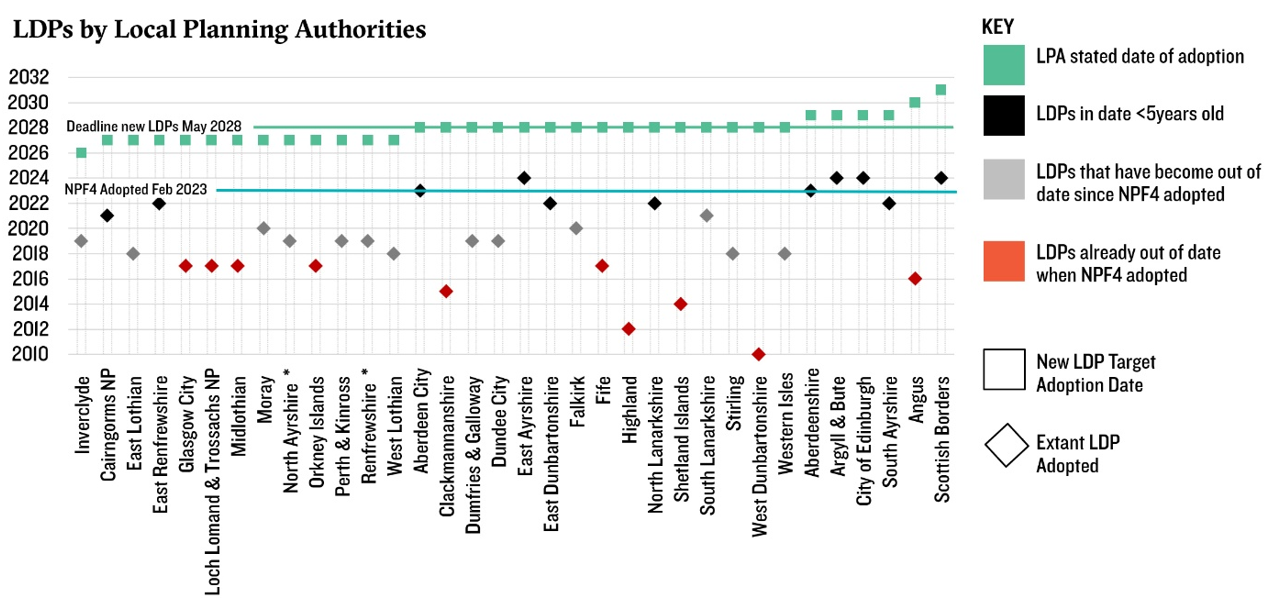

The adoption of NPF4 requires all 34 LPAs in Scotland to have new LDPs in place by May 2028

. This is essential for new housing delivery because Policy 16 of the NPF4 essentially prevents (except in limited circumstances) housing sites from being brought forward unless they are already allocated in a LDP

.

As a consequence of this shift in policy, housebuilding in Scotland has become much more reliant on the existence of up-to-date LDPs with deliverable allocations.

Unfortunately, by the end of 2026, only ten of the 34 LDPs are projected to be in date. Based on published Development Plan Schemes, six LPAs will still not have a new LDP in place by the government’s May 2028 deadline

(Figure 1):

Figure 1: Local Development Plans by local planning authorities

Figure 2 suggests that the impact of NPF4 is already clear in both housebuilding starts (down 30 percent) and planning approvals (down 66 percent) since the draft was published in 2021. The lag effect means that the current very low number of permitted units will necessarily lead to a further fall in housebuilding if not addressed. The

Mossend judgment may also have affected the success of recent planning appeals, which fell to a ten-year low of 27 percent in 2025, compared with 40 percent in 2024

.

Figure 2: Residential units granted planning permission, Scotland, by year

The Scottish consultation takes the view that, “given the scale of consented land which is already available”

, measures to increase housebuilding should focus on increasing the pace of delivery on these consented plots. However ‘the scale of consented land’ in this statement is doing a lot of heavy lifting. A system which only consents 12,000 units in a year—far short of the annual 19,700 Minimum All Tenure Housing Land Requirement (MATHLR) set out in NPF4, which itself is meant to be a bare minimum for local plan requirements

—will fall significantly short of delivering the homes Scotland urgently needs. This is the case even setting aside the deliverability and viability issues that many of these sites face, as analysed by Homes for Scotland

.

Furthermore, while it is true, as the consultation argues, that not all planning permissions will result in completed homes, it is also the case that homes cannot be built without permission. Land allocated in LDPs is a finite ‘stock’ rather than a replenishable ‘flow’ and will therefore dwindle over time without new allocations. With Scottish policy as it currently stands, new consents and new homes depend on deliverable allocations. Yet as the next section will show, our analysis of allocations made in the cohort of adopted LDPs suggests they might not be in the optimal places.

Are LDPs allocating homes in the right locations?

Given the central role of allocated sites in planning for and delivering enough homes in Scotland, these sites must not only provide sufficient theoretical ‘scale of consented land’ to support sufficient housebuilding but also be located in the ‘right places’. It is our hypothesis that allocated sites in areas with stronger housing market conditions are more likely to be deliverable than those in weaker markets. LPAs should therefore, in theory, take account for this by allocating more land in these areas.

The first consideration to note is that housebuilding in Scotland is highly concentrated in certain areas: the “Central Belt” and Aberdeen / Aberdeenshire. Unsurprisingly, in the broadest terms, this is also the case for planning approvals, where five LPAs are responsible for 43 percent of housing permissions nationally over the past decade (Figure 3).

Figure 3: Planning approvals (sites and units) by local planning authority, 2016–26

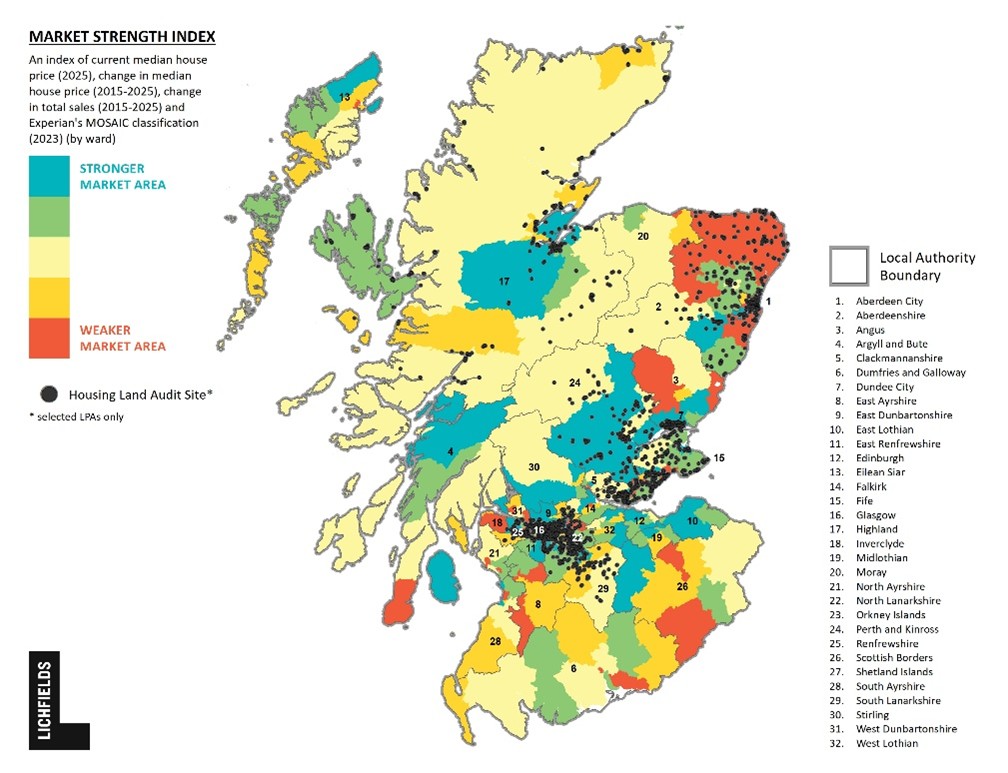

To understand the pipeline, we mapped all the allocations in LDPs (using housing land audits) for the ten LPAs with accessible data that rank highest by number of permissions. Together, this cohort is responsible for 60 percent of permissions in Scotland. We then compared the distribution of allocations to the strength of local markets by compiling a national Market Strength Index

(MSI) for housing delivery (Figure 4). The MSI compares each Scottish ward by Experian MOSAIC classification, median house price, change in median house price and in sales, producing a nationally comparable MSI score.

Stronger local markets have a high MSI score; with higher house prices and robust sales, these are considered the most viable markets.

Figure 4: Allocations in Scottish Land Audits, wards coloured by market strength

The mapped MSI clearly shows that there is significant variation across the country in the levels of housing market strength in different wards. To test statistically whether more allocations are made in stronger market areas, we plot these data in Figure 5, 6 and 7.

The number of allocations made is spread relatively evenly across wards, agnostic of market strength, i.e. there are not clearly more sites consented in stronger market areas (Figure 5).

Figure 5: Number of allocations in housing land audits per ward, by market strength index decile.

The number of units in allocations is slightly positively correlated with market strength, but remains relatively evenly spread across wards—i.e. there are not clearly more units being consented in stronger market areas (Figure 6)

Figure 6: Average number of units allocated in a ward by MSI score

The number of units allocated are skewed towards larger sites with 55 percent of units in sites of more than 250 units (Figure 7). Less than a quarter of allocated sites are under 100 units, which can act as a barrier to entry for new entrants to the market and will disproportionately affect SMEs

.

Figure 7: Total number of units in allocations, by size of individual allocation

The size of allocation sites is not correlated with market strength—i.e. there are not clearly larger sites being consented in stronger market areas (Figure 8).

Figure 8: Size of allocation sites, by MSI.

Taken together, our findings echo the 2020 analysis the Scottish Government conducted, which found that when planning authorities are assessing allocations, “The current focus is thus upon the initial deliverability of development land through assessment of constraints, and much less so upon the subsequent deliverability of development”.

These issues appear not to have been addressed, with allocations still not based on market conditions. The importance of this mismatch has been heightened following NPF4 and

Mossend.

Across our analysis we find that there is little to no relationship between where sites are allocated and market strength. A lack of regard to market strength may be leading to large allocations in areas where the market cannot support this level of activity, and smaller allocations in areas with the potential for much higher levels of housebuilding.

So where does this leave housebuilding in Scotland? Given the slow projected progress towards universal in-date plan coverage, many Scottish LPAs are now relying on out-of-date plans still having enough undelivered yet viable housing land allocations remaining in their LDPs to meet current need. To assess this situation, Figure 7 shows the breakdown of allocations by their current status in their planning journey, for the five authorities in our cohort which make this data publicly available

. The coverage is not comprehensive but these authorities account for over half the allocated units in our dataset of ten LPAs.

Figure 9: Status of allocations

60 percent of allocations have already received planning permission, with 37 percent being built out or completed and 23 percent with detailed permission or permissions in principle. With the exception of Aberdeen, Aberdeenshire and the Highlands the allocations are from LDPs that are several years old and out of date (representative of the 70 percent of LDPs forecast to be out of date by the end of the year). It is therefore a reasonable assumption that a higher share of the remaining allocations might have deliverability challenges than those that have already seen activity. This shows that the stock of remaining allocations is dwindling.

Without an alternative route to permission, an insufficient flow and range of allocated sites has the inevitable effect of slowing housebuilding, below its already critical levels. This is exacerbated by the allocations that are made being disproportionately in weaker market areas with viability challenges. The Scottish Government is right to be concerned. However, its focus on build out rates is at the expense of addressing the fundamental challenge: too few permissions are being granted to build the homes that are needed.

https://www.sfha.co.uk/our-work/still-waiting Although as of January 2026,National Planning Framework 4: delivery programme V4 assesses that 13 authorities are expected to adopt plans after this date: Aberdeenshire, Angus, Argyll and Bute, City of Edinburgh, East Ayrshire, East Dunbartonshire, Highland, Scottish Borders, Shetland Islands, South Ayrshire, South Lanarkshire, Stirling, West Dunbartonshire This was re-confirmed in the Court of Session’s May 2024 Miller Homes vs Scottish Ministers judgement, more commonly known as Mossend (covered in more detail here), https://lichfields.uk/blog/2026/february/05/will-planning-policy-in-scotland-deliver-the-homes-we-need Lichfields analysis of Landstack data https://www.gov.scot/publications/accelerating-home-building-scotland-consultation-penalties-incentives-speed-up-housing-delivery/pages/1/ https://www.gov.scot/binaries/content/documents/govscot/publications/strategy-plan/2023/02/national-planning-framework-4/documents/national-planning-framework-4-revised-draft/national-planning-framework-4-revised-draft/govscot%3Adocument/national-planning-framework-4.pdf https://homesforscotland.com/download/land-supply-analysis/?wpdmdl=6086&refresh=69dcc67ce66981776076412 Market strength index (MSI) is a composite index compiled by Lichfields incorporating local house price and change over the past decade, house sales and change over the past decade, and socioeconomic demographic profile. Homes For Scotland (2026) Scotland’s SME Home Builders In 2025 recommends “planning to support SMES to deliver more homes on small sites” Scottish Government 2020 LDPs - deliverability of site allocations: research

Disclaimer: This publication has been written in general terms and cannot be relied on to cover specific situations. We recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Lichfields accepts no duty of care or liability for any loss occasioned to any person acting or refraining from acting as a result of any material in this publication. Lichfields is the trading name of Nathaniel Lichfield & Partners Limited. Registered in England, no.2778116