I recently attended an annual conference on care homes and retirement living. It had a record-breaking attendance, cognisant of the growing awareness within the development industry of the importance of the care and retirement living sector in helping to meet our population’s diverse housing and care needs.

A message that spanned the conference is that there is growing demand but not enough supply in the sector. Policy and planning can play a fundamental role in helping to redress this imbalance, with the conference particularly noting that demonstrating need is ever more important in the planning process. It is worthwhile saying at this point that Lichfields’

Carepacity Toolkit could assist here, by evaluating the need for housing for older people, as well as assessing the potential of sites, quantifying benefits and impacts, and assisting in enabling delivery.Whilst reductions in public funding have had their own impact on the supply and delivery of care and retirement housing, it was positive to hear at the conference that more funders are investing in the sector, which in turn is generating more opportunity for different models.

Funders include UK-based and specialist funding, Asia Pacific funds, Middle East funds and US real estate investment trusts. Retirement living investors include AXA, Legal & General, Goldman Sachs and AIG, alongside Bupa and Oaktree. This wide range of institutions involved demonstrates that the market is maturing and allowing for different developer and operator models. These include the

“Propco[1]” model, whereby an investor rents a property to an operating company – an

“Opco”. This can be viewed as a safer investment route as it relies on returns from rentals without involvement in the care operation. It is a competitive model, due to a limited number of established operators resulting in potentially lower yields.

The

“Wholeco[2]” model provides an opportunity for the investor to construct a care operation, or partner with an operator. This model provides flexibility and potentially greater returns on investment, weighed against any risk derived from investing in specialist property and operating companies.

The “Smart Second Tier” model includes refurbishing modern or first generation care facilities. Here, investors support the operator with on-going investment and receive returns through increased rental income, or a share in the operating company. But refurbishment can be difficult if the facility continues operating, due to the impact of works on residents.

The range of investors and models allows for more flexible models to be provided for the end user too. This may include flexible ownership, rent-to-rent

[3] or the provision of progressive levels of care (“progressive care developments”) within a single development. Progressive care developments enable people to move in as a lifestyle choice and while still active, in the knowledge that their new home is future-proofed to respond to their potentially changing future health and care needs. There were also examples of successful, intergenerational developments discussed at the conference, for meeting the housing needs of the full age range of the population.

All of the models for this type of development align well with the National Planning Policy Framework, which states that local planning authorities should plan for a mix of housing to address the needs of different groups in the community, including older people.

However, as with any new innovation in the development sector, and as discussed in Phil Jones’ recent

blog, it is vital that both the public and private sectors increase their knowledge and evolve their understanding of care homes and retirement living, and embrace innovative approaches to meeting the country’s housing needs. This is ever more important as delivering care and retirement housing is a “people industry”, whereby different age groups have different wants and needs.

Wider social benefits that are realised from providing appropriate care and retirement housing were also promoted at the event. They include the amount of care a resident needs to receive reducing after moving in, due to the well-being benefits of enhanced social networks alongside reducing the level of worry regarding the maintenance and financial pressures of running a home.

There was also acknowledgement of the wider benefits from moves to care homes and retirement living freeing up housing stock in the general market; the knock-on effects can also help to meet the housing needs of an area.

Challenges that the sector faces within the planning system were also discussed by the majority of speakers. They included the grey area around C2/C3 use classes and financial implications relating to council policies for affordable housing provision. This is a debate that will continue, particularly if “progressive care developments” grow in popularity.

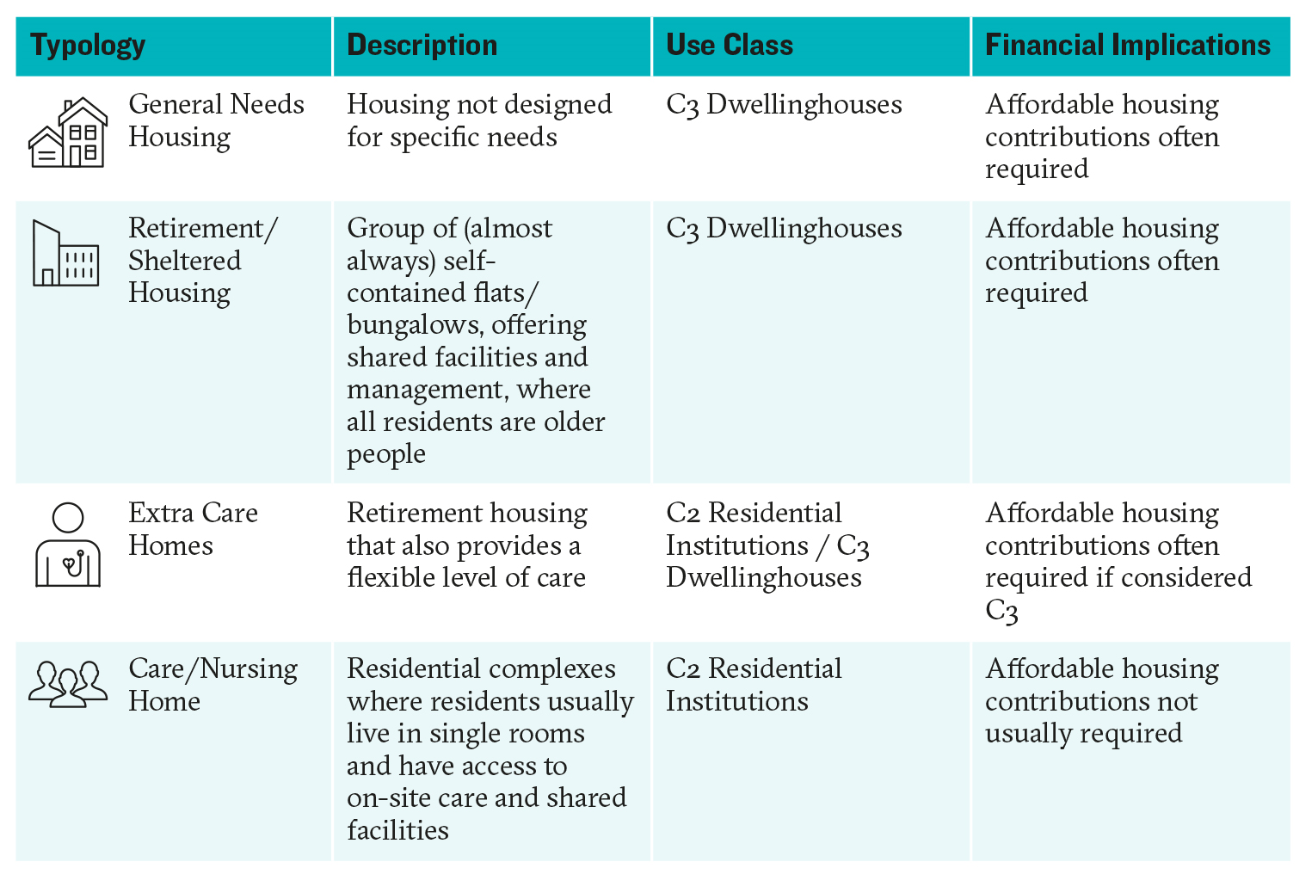

My last

blog touched on the different typologies of care and use class/financial implications, as summarised below. It is important to note that the Use Classes Order does not allow for homes to change from Use Class C3 to C2 according to the residents’ needs. It is argued by many in the industry that progressive care developments should be “sui generis”, which again has implications on affordable housing policies.

Source: Lichfields

The practicalities of providing care and retirement homes are important considerations for developers, operators, agents and planning officers, as with any development. For example, the location of such development is a key factor for residents, who need to be able to access services and facilities, and receive visitors. Additionally, as highlighted by operators at the conference, there is reliance on public transport by many care workers and therefore the ability for staff to travel to work by this mode is an important factor in locating such developments.

Whilst there are challenges for this ever-evolving sector and it is critical that national policy increases its focus on advising how local planning authorities could do much more in meeting need. It was encouraging to hear that the industry is already using innovative funding and development methods – and wanting to disseminate details widely.

To discuss Carepacity further, please get in touch:

jennifer.nye@lichfields.uk

[1] Property Company[2] Whole Company[3] Whereby the occupier rents their existing property to allow them to rent a retirement/care property.