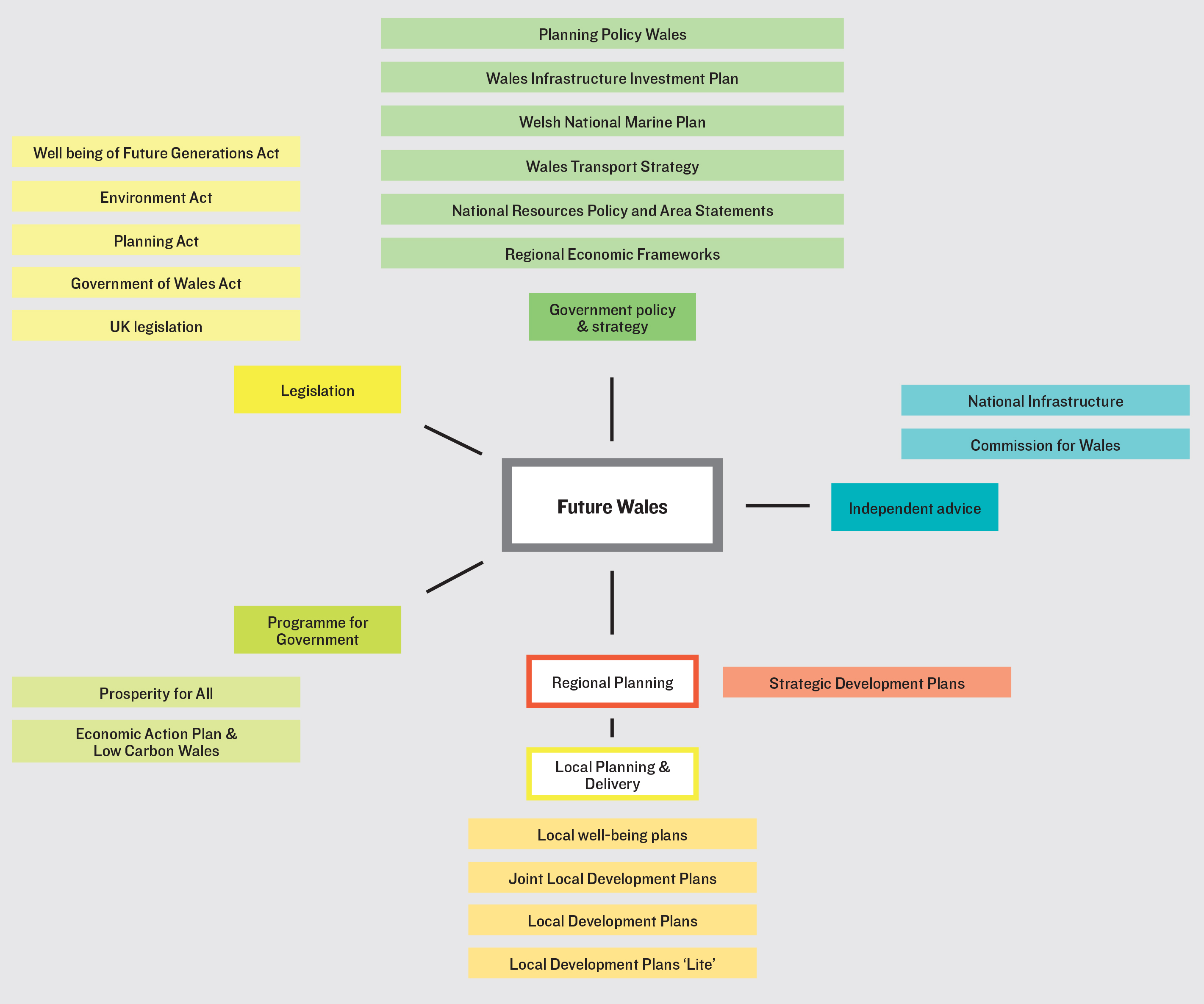

Future Wales: The National Plan 2040, described by the First Minister as a “major milestone in the ongoing development of a distinctively Welsh planning system,” was formally launched by the Welsh Government on 24 February 2021. Future Wales represents the top tier in the development plan framework for Wales, to be built on and taken forward by Strategic Development Plans (SDPs) and Local Development Plans (LDPs). It is established in legislation and is informed by, and will inform, a variety of Government strategies and plans, as illustrated in Figure one.

Figure one: Model of Future Wales influence

Source: Welsh Government, Future Wales - The National Plan 2040 / Lichfields

The timing of the publication of Future Wales, together with an updated version of Planning Policy Wales (edition 11), towards what we hope is beginning of the end of the Covid-19 pandemic, has had a key influence on elements of its content. Importantly, the final document includes a greater acknowledgement of the need to support economic growth, and this is to be welcomed.

Economic growth

Although Future Wales misses the opportunity to set out an overarching strategic economic policy for Wales, it provides support for the aims set out in the Welsh Government’s Prosperity for All: Economic Action Plan (December 2017), including:

- The development of key sectors such as advanced engineering, renewable technologies and transport;

- Growth of innovation, research and development; and,

- Support for the foundational economy, which includes care and health services, food and drink, housing, energy, construction, tourism and high street retailers.

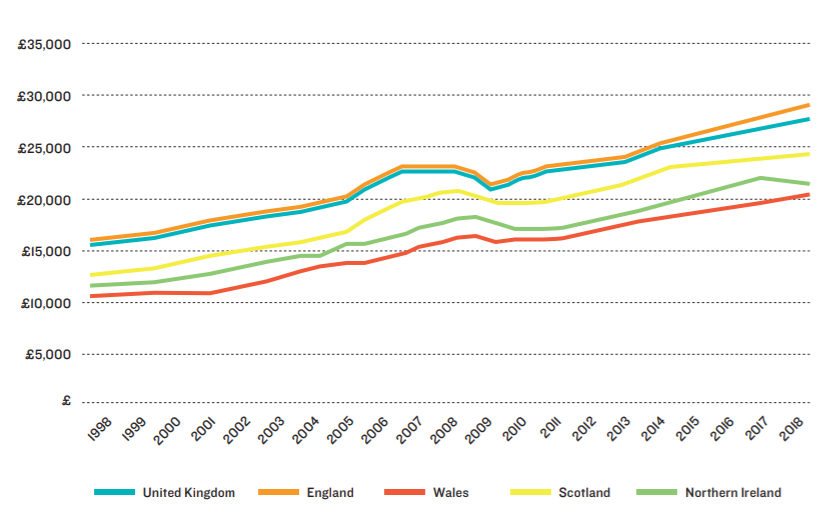

The need to “re-energise” the Welsh economy following the Covid-19 pandemic is heightened by the nation’s pre-existing economic vulnerability, especially when compared to other parts of the UK. To illustrate this point, on average GVA per worker in Wales in 2018 was £20,700 compared to the UK average of £28,700 (72% of the UK average).

Figure two: Average GVA per head of population

Source: ONS Regional Gross Value Added (2018) (provisional) / Lichfields

Future Wales supports a regional approach to economic development and provides an important link between economic strategy and planning. It notes that there are current and emerging City Deals and Growth Deals in each of the four regions across Wales and that Regional Economic Frameworks are being developed under the leadership of the Welsh Government’s Chief Regional Officers.

Critically, Future Wales sets out that these Growth Deals and Regional Economic Frameworks should assume a “reciprocal and iterative” relationship with SDPs. This connection will be important in order to ensure that sufficient land is brought forward for (the right type of) development in the right places to support and not constrain sustainable economic growth. Hence, the importance of understanding the economic context of each region, with its own particular strengths and weaknesses, when planning for development – an area of work we specialise in at Lichfields.

Placemaking and planning for a post-Covid world

There are many unresolved questions about what life will look like after Covid and to what extent previous patterns of living, working and travel will go back to the way they were. Future Wales highlights that, during lockdowns, well-designed communities played an important role in supporting health and wellbeing. It advocates that key placemaking principles, including access to parks and green space, cycle routes and local shops, will continue to be important during the post-Covid recovery.

PPW provides further policy to support this recovery, supported by the Welsh Government’s “Building Better Places” document (July 2020), which we reviewed in our July 2020 Insight Focus.

Housing

The final version of Future Wales retains its focus on affordable housing as a clear national priority but still does not acknowledge the need to increase the supply of market homes. There are significant concerns with this approach, as discussed in our November 2020 Insight Focus. It is important to recognise the value of private housing, not just in terms of providing somewhere to live but also in the economic and social benefits of good quality homes in well-designed communities (reflecting Future Wales’ focus on placemaking). It should also go without saying that the delivery of private housing is a major driver for the provision of affordable homes.

The final version of Future Wales does, however, recognise that there is a need to “think about how we will retain and attract young people to all parts of Wales” in the context of the ageing population. This is absolutely vital in order to sustain services as well as providing the needed labour force to support economic growth. Furthermore, the increased focus on universities in this final version of Future Wales should also be reflected in the aim to retain graduates and skilled workers more generally.

Providing a sufficient number of homes in the right locations will be key to achieving this aim, and housing requirements in SDPs and LDPs must not be constrained by the past demographic trends that are embedded within the Welsh Government’s national and regional estimates of housing need. Indeed, Future Wales clearly states that these estimates do not take any account of future policies and states that “it is expected the housing requirements will differ from the estimates of housing need.”

Urban growth and regeneration led by the public sector

Future Wales sets out that the public sector will need to play a greater role in assembling land and enabling development in order to achieve the Plan’s growth and regeneration aspirations. Intervention by the public sector is certainly needed in order to unlock many brownfield sites for development, some of which have lingered in the planning system for years. However, there are widely held concerns that public funding is vastly inadequate to enable delivery where it is most sorely needed.

Furthermore, the role of the private sector should be recognised, including developers of all sizes, bringing a wealth of skills, experience and investment potential and offering opportunities for partnership working to bring forward regeneration schemes that are currently unable to progress.

The future starts now – or does it?

While it is positive to see the top tier of the new planning system now in place, there are noticeable gaps at the lower levels – meaning that in many areas development is currently unable to come forward.

The SDPs for each region will be led by Corporate Joint Committees (CJCs), as set out in the Local Government and Elections (Wales) Act (2021). The CJCs will be comprised of the leaders of each local authority together with any additional invited representatives from councils or other organisations. It is not anticipated that the CJCs, once convened, will reach Delivery Agreement stage until 2022. Hence, it will be several years before the first SDP is adopted.

It is therefore vital that new and revised LDPs come forward to enable needed development in the medium term, guided by Future Wales and bringing forward deliverable allocations to meet the needs of the nation. Short term solutions are also needed, recognising that plan making is an inherently slow process. Critically, eight of the 25 local planning authorities in Wales have LDPs that are due to expire this year and a further two do not have an adopted LDP at all. Sustainable development that is in accordance with Future Wales and PPW should therefore be supported in advance of the adoption of the next round of LDPs.

Future Wales is presented as a “lever” to deliver real change – responding to the climate emergency, re-energising the economy and supporting opportunities for a better Wales “with every mechanism at our disposal”. With the national plan now in place and the hope of a post-Covid recovery, it is high time to activate the mechanisms available within the planning system to deliver this needed change.