As the UK reaches past what will hopefully be the only peak of the COVID-19 pandemic, questions are being asked about what the ‘new normal’ will be post-pandemic. These questions include how long some form of social distancing will be required, where will we work in the future, and how we will get there.

Pre-pandemic, it was common for many people that work in the major commercial hubs of London such as Canary Wharf, the City of London and West End to commute via mass public transport services (e.g. London Underground, suburban railways and buses). The importance of these services pre-pandemic is reflected in statistics produced by the Office for Rail and Road (ORR) and Transport for London (TfL) that measure usage of the railway network and London Underground.

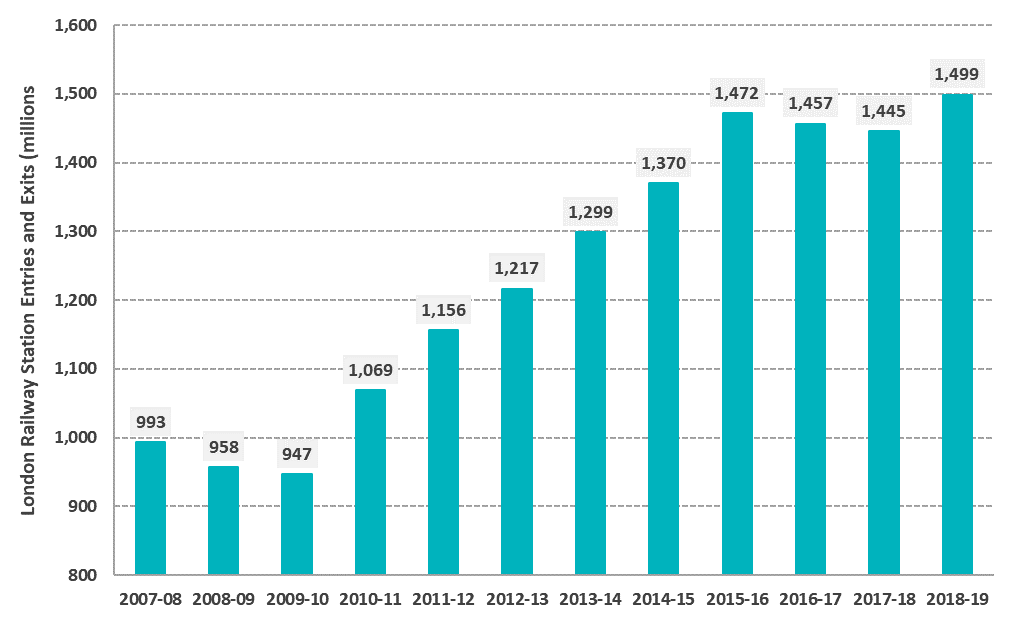

ORR statistics show that in 2018/19, there were 1,499 million entries and exits at above-ground railway stations within London, representing an increase of 50% over the number of entries in exits in 2007/08 (993 million)

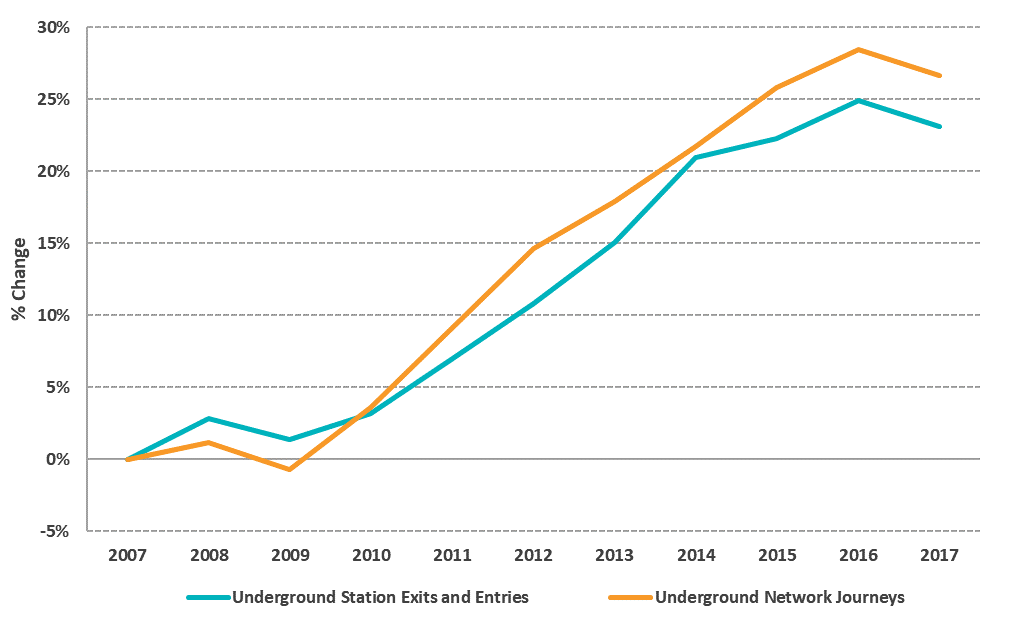

[1] (see Figure 1). Across the London Underground network, TfL estimates that there were 2,946 million entries and exits and around 1,358 million journeys in 2017, which represent increases of 23.1% and 26.7 respectively from 2007

[2] (see Figure 2). However, it is worth noting there had been a slight decrease in exits and entries and journeys between 2016 and 2017, which impacted upon TfL’s income

[3].

Figure 1 London Railway Station Entries and Exits, 2007/08 – 2018/19

Source ORR (2020) / Lichfields analysis

Figure 2 % Change in London Underground Entries and Exits and Network Journeys, 2007-2017

Source TfL (2020) / Lichfields analysis

The pandemic has, of course, radically impacted on passenger numbers for 2020 as the government introduced lockdown measures. The railway network is currently running at around 10% to 15% of pre-pandemic capacity because of social distancing measures and fewer services being run

[4], while TfL estimates the London Underground with social distancing enforced will have the capacity to carry 13% to 15% of the normal number of passengers when running a full service

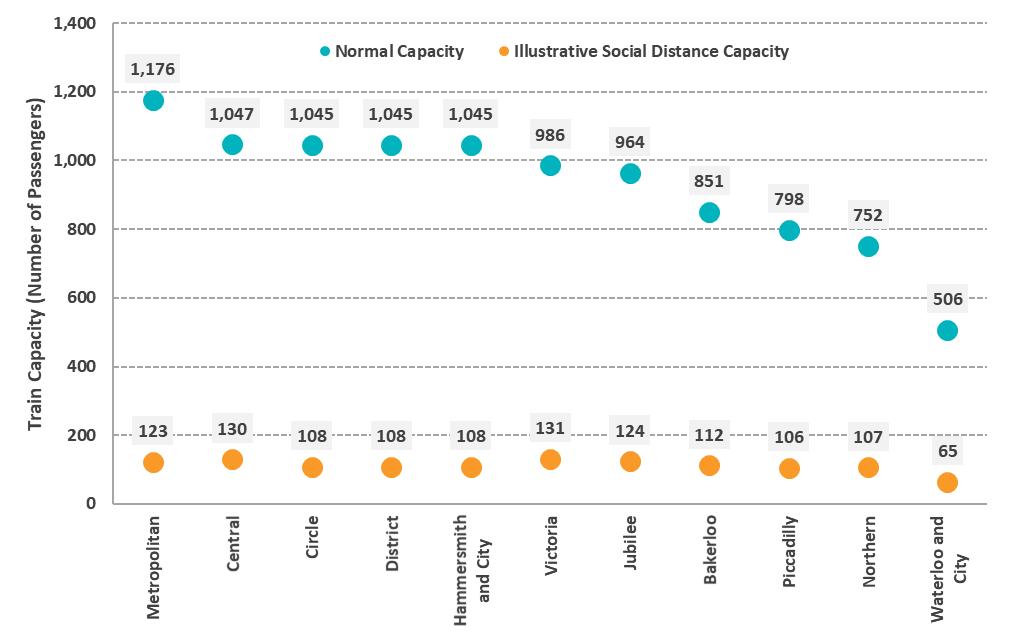

[5]. This is further illustrated in Figure 3 which shows the difference between the normal capacity and an estimated enforced social distancing capacity of a train on each London Underground line.

Figure 3 London Underground Line Train Normal Capacities and Illustrative Enforced Social Distancing (1 metre) Capacities

Source: Lichfields analysis[6]

Note the illustrative capacity of trains on each London Underground line was calculated by taking the length of a train car, multiplying the length by the number of cars in each train and then dividing by one metre, which will be the minimum social distance recommended by the UK Government as of 4th July 2020. The actual social distancing capacity of trains on each line may vary from these illustrative estimates as the length of each train is the primary input and the calculations do not take account of how the width of a train could be used to boost capacity and the effect of household groups travelling together.

Working from home where possible has become a common occurrence and is clearly shown by the Office for National Statistics (ONS) Lifestyle and Opinions Survey dataset, which indicates 44.1% of people surveyed at least partly worked from home between 24

th April and 3

rd May 2020

[7]. This represents a significant increase from 2019 when 14.1% mainly worked at their own home, same grounds or buildings, or used their home as a base of operations

[8].

As the workforce becomes increasingly used to working from home, there is the potential for it to become a more common occurrence post-pandemic as workers become used to a different lifestyle. Initial indications of this include the results of a survey undertaken by transport consultancy Systra, who found 17% of full and part-time workers believed they would work from home more once travel restrictions are lifted, and 27% of rail commuters said they would make fewer public transport trips

[9]. The initial actions of some businesses also suggest the potential change, with Twitter offering the opportunity for UK staff to ‘work from home forever’.

[10]This potential shift in where people work could have significant implications not just for the organisations that run public transport services, who are already faced with further large drops in revenue because of the pandemic

[11], but also how the Mayor of London and Greater London Authority (GLA) plan to focus development around existing public transport nodes and new public transport schemes (e.g. Crossrail 2 and the Bakerloo Line Extension). If people work from home more often and require public transport less, demand for services such as the London Underground could decrease, thereby introducing the question of whether there is also a need for the same level of new public transport infrastructure that adds new capacity to the system.

Living close to public transport nodes could also become a less important factor influencing where renters and homeowners choose to live, that might undermine to some extent the attractiveness of high-density new dwellings that are delivered under the premise of providing workers with an easy commute via public transport. The May 2020 RICS Residential Market Survey indicates this could occur – with 78% of respondents feeling there would be a decrease in the attractiveness of tower blocks, while the desirability of having a garden/balcony, being located near to green space and greater private/less communal space would increase (81%, 74% and 68% respectively)

[12] – although respondents did not anticipate the desirability of being located near to a transport hub would change.

But the implications of any such potential shift in buyer attitudes could be significant – Table 2.1 of the Intend to Publish London Plan indicates 78,000 new homes could be accommodated within Opportunity Areas along Growth Corridors that include the Bakerloo Line Extension, Crossrail 2 South and Crossrail 2 North

[13]. There is logic to why the Mayor and GLA have planned in this way; improvements in public transport have a history of bringing development forward in London. For example, the success of Canary Wharf as a business location was helped by the completion of the Jubilee Line Extension, and the Crossrail Property Impact and Regeneration Study (2018) indicates consent was gained for 90,599 residential units around Crossrail stations between 2008 and 2016

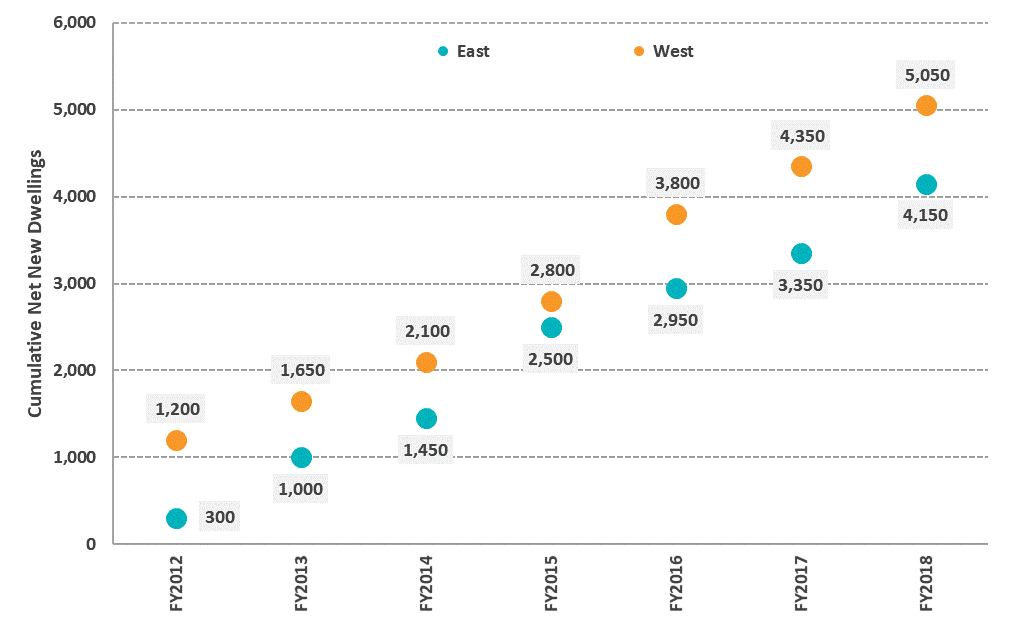

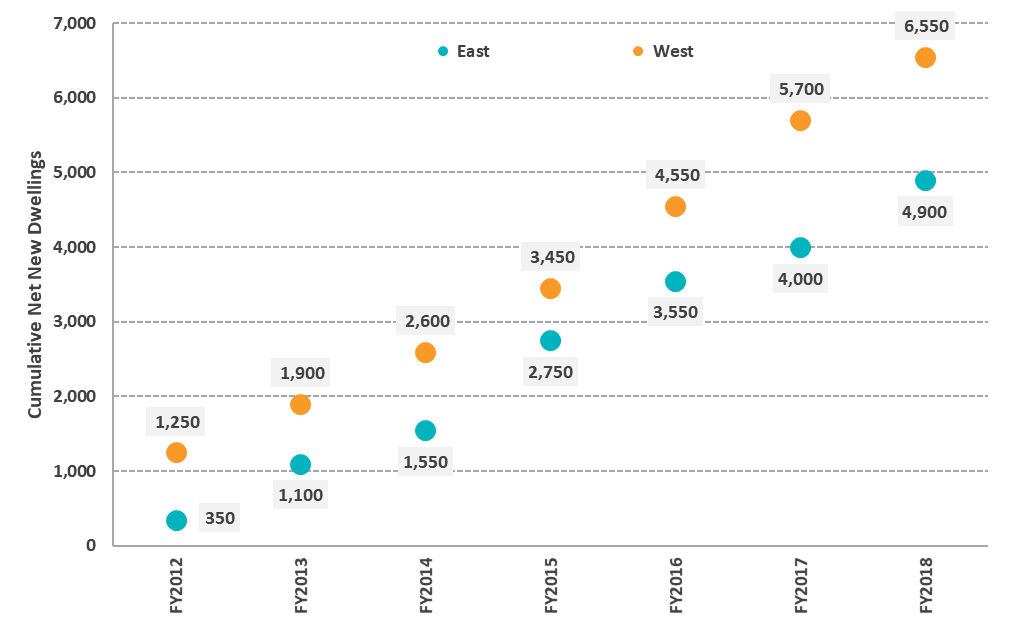

[14]. Furthermore, analysis of London Development Database (LDD) completions data by Lichfields shows there have been considerable net gains in dwellings around Crossrail stations on the above-ground sections of the Great Western Mainline and Great Eastern Mainline (see Figure 4 and Figure 5 below)

[15].

Figure 4 Cumulative Net Dwelling Completions within 0.8km of London Crossrail Stations on the Great Western Mainline and Great Eastern Mainline by Financial Year

Source: GLA (2020) / Lichfields analysis

Figure 5 Cumulative Net Dwelling Completions within 1.0km of London Crossrail Stations on the Great Western Mainline and Great Eastern Mainline by Financial Year

Source: GLA (2020) / Lichfields analysisNote that all numerical values in Figure 4 and Figure 5 are rounded to the nearest fifty. The stations included in the analysis for the above-ground sections of the Great Western Mainline and Great Eastern Mainline within London are as follows:East: Maryland; Forest Gate; Manor Park; Ilford; Seven Kings; Goodmayes; Chadwell Heath; Romford; Gidea Park; and Harold Wood.West: West Drayton; Hayes and Harlington; Southall; Hanwell; West Ealing; Ealing Broadway; and Acton Mainline.

Planning policy in London may need to adapt to find a new way forward. Essentially, planning can be viewed as a market intervention designed to deliver better places in the long-term than if short-term market forces were left unchecked; however, in the current circumstances, flexibility in policy may be of a benefit to enable quick interventions so that long-term ambitions do not go substantially off course. To inform whether and when quick interventions may be required, the Mayor and GLA could consider initiatives such as:

- Monitoring the use of public transport in collaboration with organisations such as TfL and train companies to identify whether or not commuting patterns permanently change as a result of the pandemic;

- Investigating how forms of private transport (e.g. bicycles and motorcycles) could be integrated into the backbone of planning policy to enable the same or better outcomes;

- Engaging proactively with different stakeholders and organisations to gauge market sentiment; and

- Analysing the latest data and intelligence to keep up to date with changing economic and social conditions.

The Mayor and GLA have the capability to undertake such initiatives, and it will be interesting to watch what they do in the light of the current pandemic and recent response from the Secretary of State on modifications to the London Plan in terms of post COVID-19 planning policies.

[1] Office for Rail and Road (ORR), (2020); Station Usage 2018-10 Time Series Data (revised March 2020)[2] Transport for London (TfL), (2018); Multi Year Station Entry and Exit Figures[3] https://www.wired.co.uk/article/tfl-finances-transport-for-london-deficit-passenger-numbers[4] https://uk.reuters.com/article/uk-health-coronavirus-britain-railway/with-one-way-systems-and-floor-markings-britain-increases-rail-services-idUKKBN22U0KC[5] https://tfl.gov.uk/info-for/media/press-releases/2020/may/tfl-announces-plan-to-help-london-travel-safely-and-sustainably[6] https://www.whatdotheyknow.com/request/239641/response/590412/attach/3/RS%20Info%20Sheets%204%20Edition.pdf[7] Office for National Statistics (ONS), (2020); Opinions and Lifestyle Survey (COVID-19 Module)[8] ONS, (2020); Homeworking in the UK Labour Market[9] https://www.systra.co.uk/en/newsroom-37/latest-news/article/public-transport-passengers-say-they-could-make-fewer-trips-after-pandemic[10] https://www.bbc.co.uk/news/technology-52628119[11] https://uk.reuters.com/article/uk-health-coronavirus-london-transport/london-transport-operator-secures-emergency-government-funding-bbc-idUKKBN22Q30A[12] RICS, (2020); May 2020: UK Residential Market Survey[13] Greater London Authority (GLA), (2019); The London Plan – Intend to Publish: Spatial Development Strategy for Greater London.[14] Crossrail, (2018); Crossrail Property Impact and Regeneration Study[15] GLA, (2020); London Development Database – Housing Completions Unit Level

Image credit: Claudia Soraya via Unsplash