Last year, in the early weeks of the initial lockdown, our colleague Matthew Spry wrote a

blog pondering the impact of the pandemic on housing supply and delivery. Would the planning policy response be ‘dove’ or the ‘hawk’? In other words, would the Government cut Local Planning Authorities (LPAs) some slack on under delivery for reasons clearly not within their control or look at the situation as real households having their housing needs going unmet requiring corrective action.

In February 2021, we got perhaps the first (baby) dove with the publication of the 2020 Housing Delivery Test (HDT). One month’s worth of requirement was taken off the 2019/20 monitoring year to account for the initial lockdown which started in March 2021

[1].

Last week, Rt Hon Christopher Pincher MP (Minister of State for Housing) used a Written Ministerial Statement (‘WMS’)

[2] to announce further changes to the upcoming 2021 Housing Delivery Test (‘HDT’). This time, a

“four month adjustment” will be made to the 2020/21 monitoring year; deducting “

122 days to account for the most disrupted period that occurred between the months of April to the end of July”. Does this signal the release of another dove with implications for years to come? The answer, as ever, will be one of perspective – but ultimately its impact will depend on whether this one year 33% reduction in the HDT is greater or less than the fall in housing delivery for 2020/21 genuinely and directly attributable to Covid-related disruption.

What will be the effect of the WMS changes to the 2021 HDT?

The two Covid-based discounts to the housing requirement means the HDT will be made on an assessment of supply against 31 months of housing requirement not 36. This is a reduction of 14% and will last for the 2021 and 2022 HDT until the 2019/20 monitoring year falls out of the three-year assessment period. By then, for the 2023 HDT, the discount will still be the four months’ worth deduction made to the 2020/21 monitoring year; an 11% overall discount across the three-year period.

The key takeaway here is that this amendment will affect the next three tests and will influence planning for new homes until at least November 2024. This would be the point at which the 2024 HDT should be published which would not assess delivery from a Covid-affected year.

This approach is being taken despite the strong

bounce back of housebuilding activity already being seen; Q1 2021 starts were the highest in 15-years, whilst the 12-month figure to end of Q1 2021 was only 6% below the equivalent pre-pandemic 12-months to end of Q4 2019. Pent-up demand for building is already helping to dampen any long-term direct effects from Covid on supply. Meanwhile, Government is running short of its ambition to achieve 300,000 homes per annum by the mid-2020’s. It remains to be seen whether this lightening of the foot from the HDT pedal will hinder meeting that objective; will it send the right signals in a critical period for putting in place the planning permissions to deliver those 300,000 homes per annum in mid-2020’s?

This leads to an important consideration…

Is there a rationale for a 5-month discount due to Covid?

No one would dispute that the house building industry struggled in the initial lockdown last year when many sites were mothballed. It also faced challenges coming out of lockdown as social distancing requirements affected output. However, was the impact of Covid equivalent to a combined five-month hiatus in housing supply?

At this stage it is difficult to say because the national net additional dwellings statistics have not been released. However, the following observations can be made:

- As a starting point, the lockdown was formally made on the 23rd March and Government lifted restrictions on people who could not work from home on the 10th May (less than two months of full closures). Based on trading updates, most housebuilders were reporting they were back up to a good level of capacity by May-July last year. (e.g. Berkeley noted that production capacity had fallen to 40% but had by June increased to 80%[3], Bellway in June 2020 noted they were back constructing 230 of their sites[4]; and Barratt stated in July 2020 they were at c.75% of pre-covid levels[5]);

- In the final quarter of 2020/21 (Q1 2021) there were the highest number of new build completions in over 20-years, 4% above the same period in the 2019/20 year, with new build housing completions just c.10% lower in 2020/21 than the previous year[6];

- Housebuilder releases show a return to pre-pandemic levels. By way of example Barratt in FY20 (covering the year to 30 June 2020 and most of the pandemic impacted period) completed 12,604 homes, compared to 17,865 in FY19 and 17,243 in FY21, indicating the whole the pandemic created a c.29% effect on business (c.3.5 months of output)[7]; and

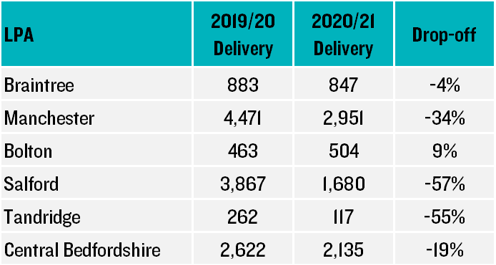

- Looking at a few LPA examples (see table) where monitoring figures are already released for 2020/21 completions figures have ranged from +9% to -57% on the previous year, with an average drop-off of around a third. Of course, these six LPAs may not be representative for all of England but might support the four month discount for 2020/21 as being in the right ball park.

What next: The ‘hawk’ vs ‘dove’

Fewer homes were undoubtedly built in 2020/21 due to Covid-19 than would have otherwise been the case. The actions or inactions of the LPAs were not responsible for that dip. Were one to view the HDT as a ‘penalty’, then cutting LPAs some slack (and with a combined five month discount that is likely to more than offset the reduced period of building) will make sense because it reduces the potential for LPAs to feel a sense of injustice (which in turn might undermine confidence in the HDT policy). But if one were to see the HDT not as a ‘stick’ or punishment but as mechanism to temporarily bolster housing supply to make good past shortfalls (however they arose) then the five months makes less sense.

In any event, the housing crisis remains and the need for homes remains, and indeed demand is stronger, than ever. UK average house prices had increased by 13.2% over the year to June 2021; the highest annual growth rate the UK has seen

since 2004. This rise is due to a range of factors, but homes are now much less affordable in many areas than they were before the pandemic.

In practice, the adjustment to the HDT measure will likely mean some areas do not see measures in place to help boost supply, even though far fewer homes have been delivered due to Covid

[8]. This position will last until at least November 2024; a point at which the economy, the housing supply, and the housing need situation may be different. The relaxation may be perceived as ‘fair’ (particularly given the current political context), but it could be seen as a missed opportunity to align with the Government’s stated objective of ‘significantly boosting the supply of homes’.

The adjustment also raises further questions as to whether the HDT is a hard and fast set of rules (with the ‘rulebook’ to back it up) or open to requests for relaxations for other reasons. If Covid-19 (undoubtedly a

force majeure) warrants an adjustment to the HDT, then what about other exceptional or macro-economic factors beyond LPAs control? For example, current labour supply and materials shortages are putting downward pressure on construction activity

[9] – particularly for smaller developers; will the Government now be asked by LPAs to make an adjustment for 2021/22 to reflect this too?

The relaxation to the HDT may mollify some LPAs who might feel aggrieved if their area fell below the HDT thresholds and saw them subject to a 20% buffer or the tilted balance through no fault of their own, but as a ‘doveish’ gesture, it does nothing to help people needing homes and the Government in increasing supply to meet its ambitions.

[1] This might be viewed as generous given the initial lockdown was enforced from 23rd of that month. [2] The WMS can be found here[3] https://www.berkeleygroup.co.uk/media/pdf/q/f/FY20_Results_Announcement_June_2020.pdf[4] https://www.bellwayplc.co.uk/media/1738/2020-04-30-covid-19-update-final.pdf[5] https://www.barrattdevelopments.co.uk/media/media-releases/pr-2020/pr-06-07-20[6] https://www.gov.uk/government/news/home-building-stats-show-continued-increase-in-starts-and-completions-despite-pandemic[7] https://www.barrattdevelopments.co.uk/media/media-releases/pr-2021/pr-14-07-2021[8] Although our research report on the HDT – Effective or Defective – found that in four out of five cases, the authorities that fail the most punitive threshold (application of para 11(d)) are those that cannot demonstrate an up to date Five Year Housing Land Supply, meaning the tilted balance has already been triggered via another avenue. In addition, around half of the authorities that fail this threshold are significantly constrained by Green Belt and/or other NPPF Footnote 7 designations, meaning that the ‘very special circumstances’ (or similar) required to justify new housing development will, in many cases, over-ride the tilted balance.[9] As reported here