The

English Devolution White Paper, published in December 2024, signalled a profound change in approach to local economic growth across England; in terms of geography, governance and delivery of public services.

As promised within their election manifesto, the Labour Government has embarked on a joint programme of devolution reform and local government reorganisation as follows:

- Local government reorganisation – replacing the current two-tier system of counties and district councils with unitary councils across the country, to result in fewer, larger authorities.

- Widening devolution across England – to include universal coverage in England of Strategic Authorities with greater powers and funding to influence local economic growth.

Work is now well underway to determine what this new devolution landscape will look like. A number of devolution ‘front runners’

have already been announced, and Government has committed to delivering an ambitious first wave of local government reorganisation in this Parliament. They believe that devolution is fundamental to achieving its overarching priority for growth, by pushing down power, control and funding for key economic policy levers such as transport, skills and planning to areas that are best placed to make these decisions.

The scale of the administrative and geographical change associated with this “devolution revolution” and local government reorganisation is significant and has been described by many Council leaders as a “once in a lifetime opportunity”

[1]. Inevitably, this is likely to result in a hiatus in local economic growth activity within those areas undergoing change as new structures are put in place. Growth momentum could be impacted over the short term as funding systems change, priorities are re-assessed, and new relationships and growth partnerships are forged.

Notwithstanding the immediate turbulence this will cause, those areas that can mobilise to embed themselves within the new regime as quickly as possible stand the greatest chance of capitalising on the opportunities it presents and achieving their economic potential.

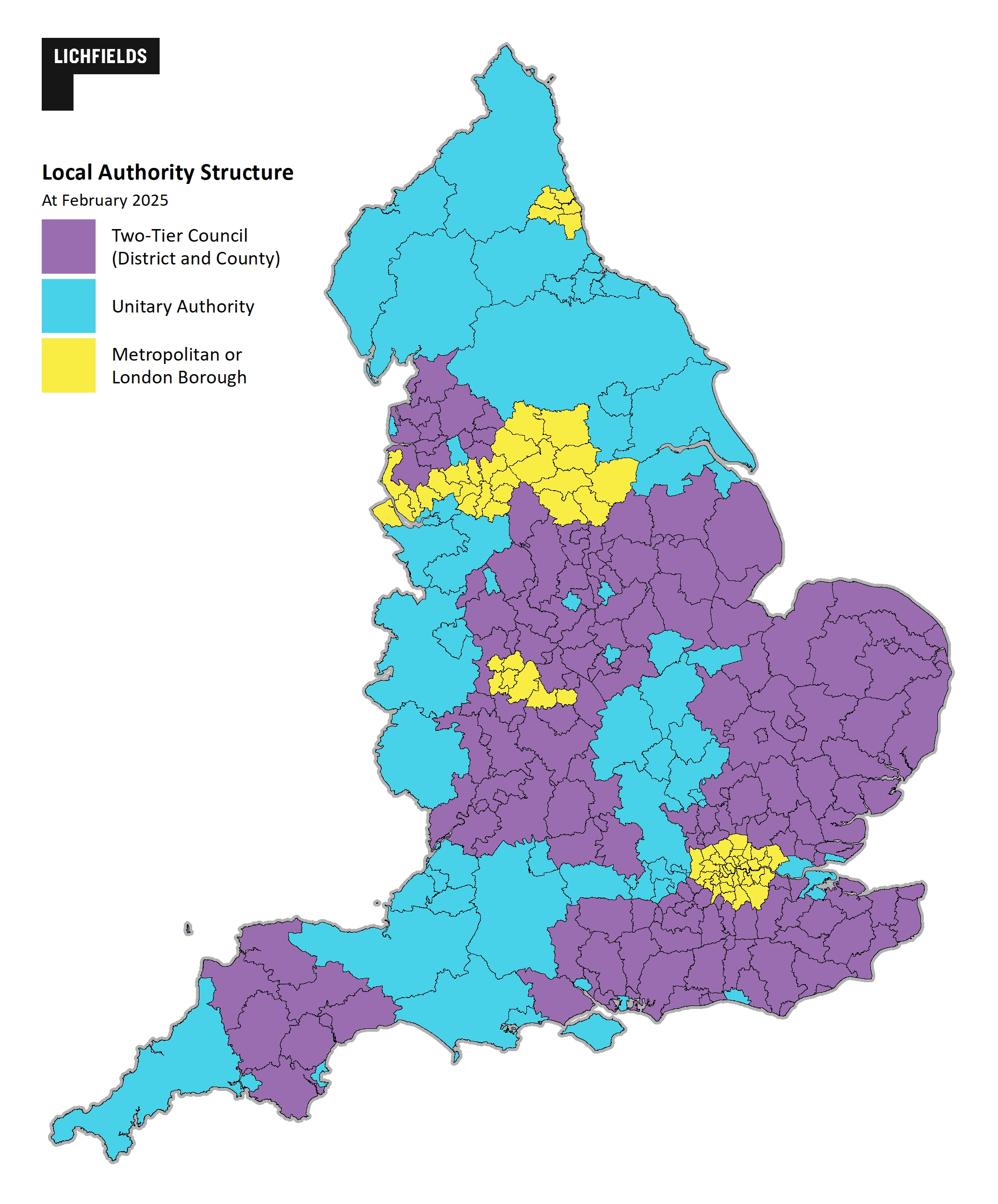

Where is local government reform taking place?

There are currently 132 unitary local authorities across England, collectively covering 71% of the population

[2]. The map below – illustrating the existing local authority structure – shows that the geographical focus for local government reorganisation is on large parts of the East and West Midlands, East Anglia and the South East.

Source: Lichfields

The Government has specified that unitary authorities should have a population of at least 500,000, whilst also reflecting sensible, functional economic geographies. This means that some existing unitary authorities will need to merge (for instance Leicester, Stoke-on-Trent and Plymouth all have a population of less than 500,000) and proposals have been invited from “

those unitary councils where there is evidence of failure or their size or boundaries may be hindering their ability to deliver sustainable and high-quality services to their residents[3]”.

Interim plans for local government reorganisation have been requested by 21 March 2025, followed by full proposals by 28 November 2025. So, we should expect to see new unitary geographies emerging soon, and with it, a new administrative geography for England. Clearly, this will have widespread implications in terms of how we plan for, fund, deliver, and scrutinise local economic growth and development activity.

For some places, this will involve an immediate change to the composition of their ‘local economy’ (in terms of profile, sectors, USPs, challenges etc) as they extend across a wider geographical area. The range of locally available assets, levers and opportunities to support economic growth objectives may also look significantly different. And of course, the local political environment may change, and with it, aspirations and attitudes towards growth.

How might devolution influence economic growth strategy across England?

Devolution will see the coverage of Strategic Authorities across the whole of England for the first time. A Combined – or ‘Strategic’ – Authority is a legal body that enables a group of two or more councils to collaborate and take collective decisions across council boundaries. They cover issues that require strategic oversight of the entire region and have responsibilities, and funding, to deliver a range of economic development activity including skills, employability and business support, amongst other related areas such as strategic planning and transport.

Those areas with existing Mayoral Combined Authorities and non-Mayoral Combined Authorities will be handed greater powers and funding (weighted towards Mayors), while others will become part of newly formed Strategic Authorities (with or without a Mayor). Government has set a series of geography and governance criteria, to include a combined population of at least 1.5 million and “sensible” economic geographies that reflect functional economic areas (such as travel-to-work patterns and local labour markets).

Six ‘front runner’ areas were announced in early February as part of the government’s

Devolution Priority Programme; Cumbria, Cheshire & Warrington, Norfolk & Suffolk, Greater Essex, Sussex & Brighton, and Hampshire & Solent. Devolution agreements have also progressed in Greater Lincolnshire, Hull and East Yorkshire, Devon and Torbay, and Lancashire. Discussions are ongoing elsewhere.

So, what do these emerging devolution geographies

[4] look like in economic terms, how do they compare with ‘existing’ devolved areas, and how might this new scaled up geography influence economic growth strategy going forward?

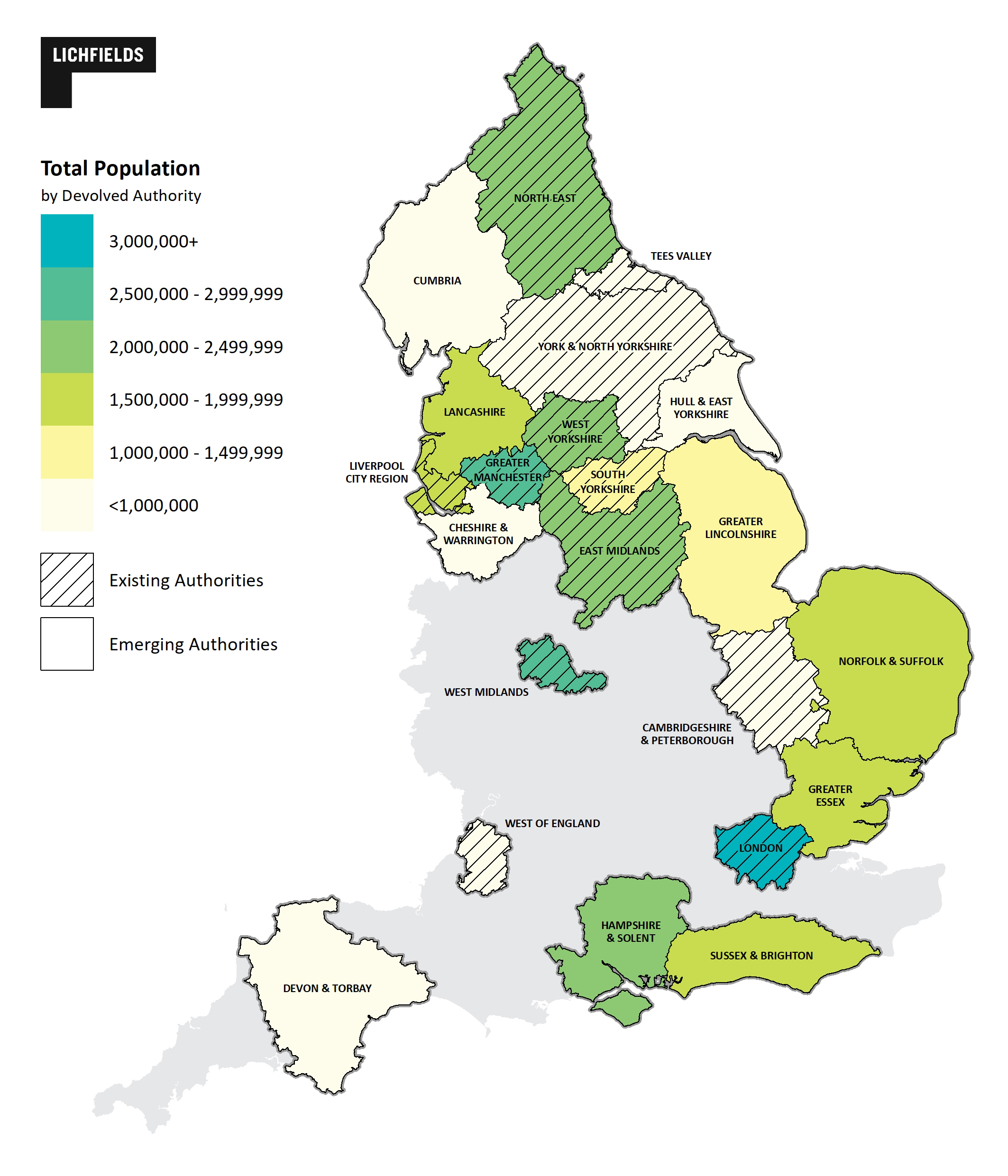

Population

The total population associated with existing and emerging devolution geographies varies considerably. Given that the country’s largest urban centres (London, Greater Manchester, West Midlands) already have Mayoral Combined Authorities in place, it is perhaps unsurprising that the emerging devolved authorities tend to have smaller overall populations. Cumbria accommodates the smallest population (c.505,000) and Hampshire & Solent the largest (c.2,036,000).

Source: Lichfields analysis, drawing on ONS Mid-Year Population Estimates (2023)

Interestingly, many areas (both existing and emerging) have a combined population that falls below the government’s 1.5 million threshold.

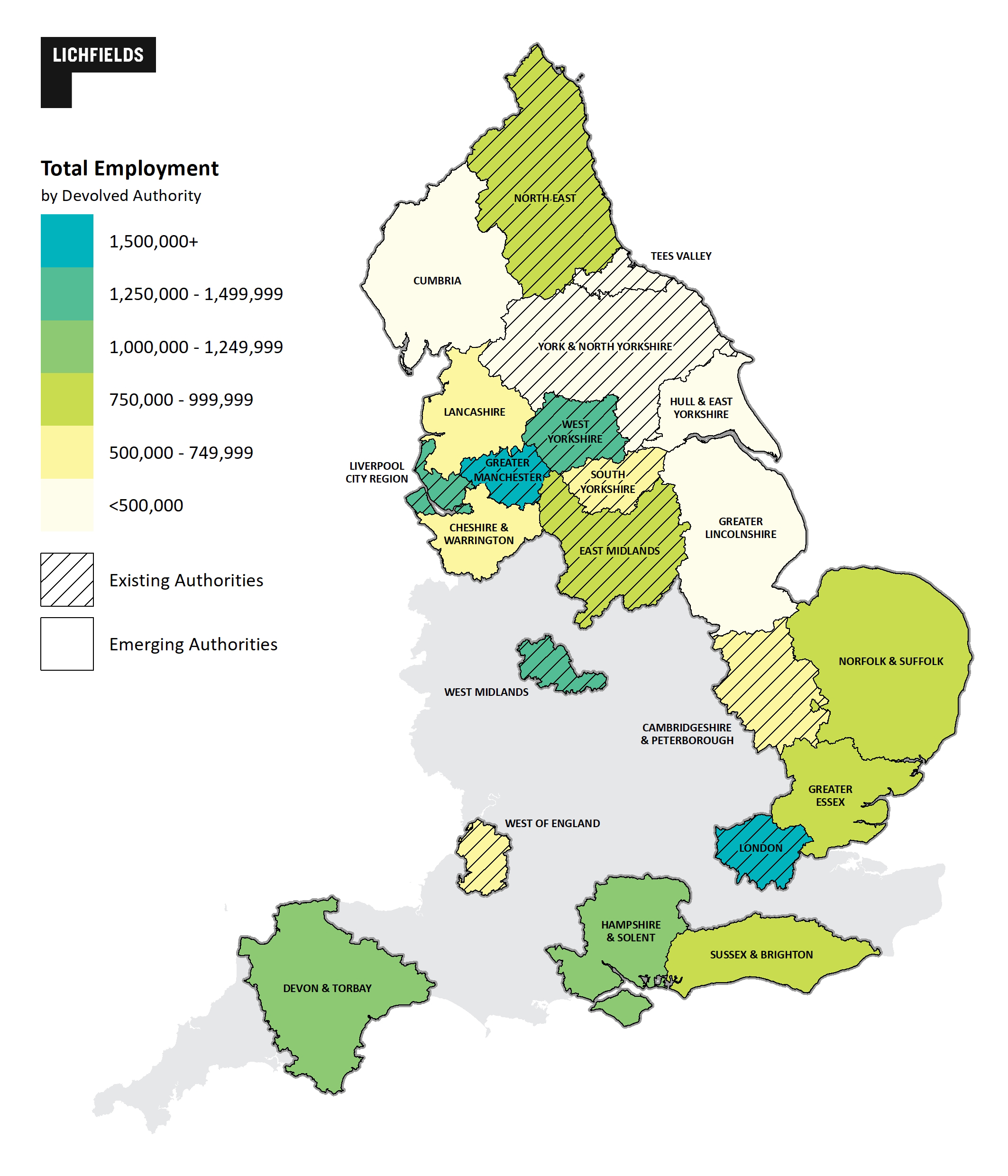

Economy

A similar pattern is evident when considering the overall size of devolved area’s economies in employment terms, i.e. with the large urban conurbations already under devolution accommodating the largest economies. A north-south divide is also evident, with emerging authorities in the south of England generally characterised by larger employment bases than areas such as Hull and East Yorkshire, Cumbria and Greater Lincolnshire, reflecting the relative concentration of larger economic centres.

Source: Lichfields analysis, drawing on Experian (2024)

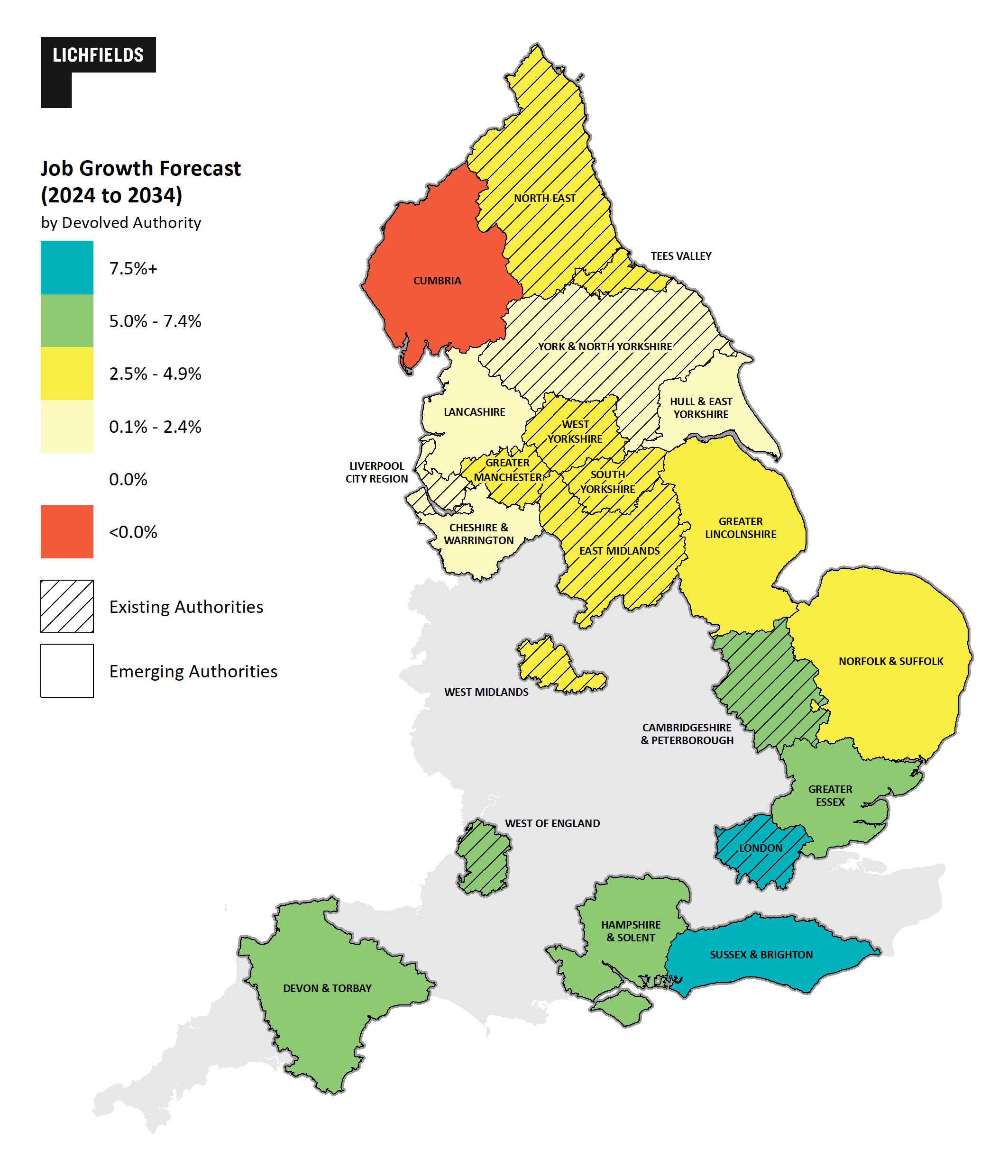

Growth Potential

This north-south divide is emphasised further by forecast job growth over the next ten years, which indicates variable economic performance across devolved areas under a ‘policy off’ scenario. This underlines the scale of the challenge for greater devolution to unlock regional growth, and the continued need for inherently different growth strategies in different places.

Source: Lichfields analysis, drawing on Experian (2024)

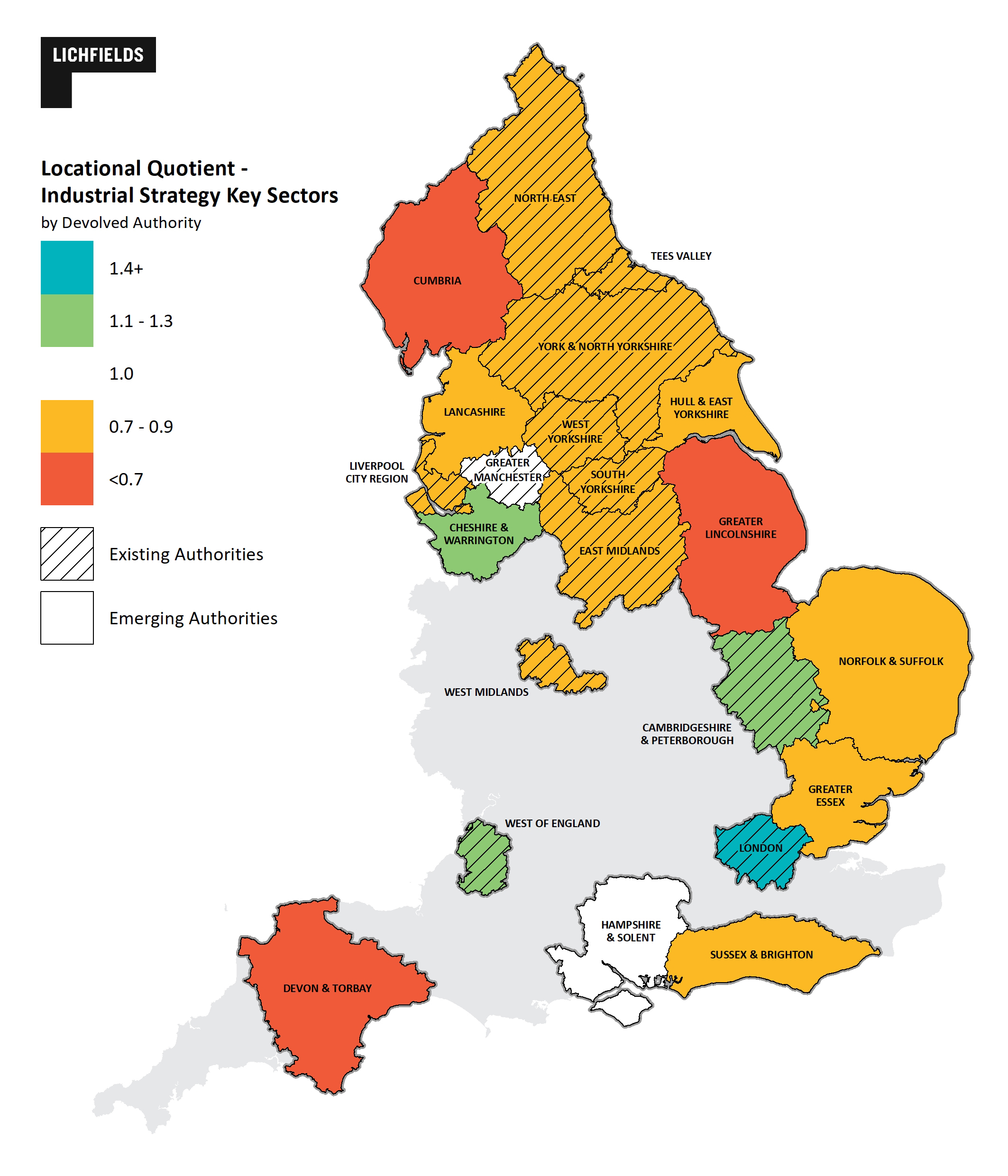

Our final map provides an indicative analysis of future growth potential across England’s existing and emerging devolution geographies by considering the relative representation of the

Industrial Strategy’s eight growth driving sectors

[5] within their existing economic base

[6].

Source: Lichfields analysis, drawing on ONS BRES (2023)

This suggests that the current devolution landscape is not particularly well represented across these growth driving sectors (with the notable exception of Greater London). Strategic Authorities have been tasked with preparing Local Growth Plans that identify how growth in their region will be aligned to and support the Industrial Strategy, so early-stage focus will need to be on how they can make the most of their unique sector strengths to demonstrate their relative contribution.

What’s next?

As devolution and associated local government reform continues “at pace” over the coming months, it will be interesting to see how remaining areas of the map are filled, and how the various authority structures begin to take forward Government’s ambitious mandate for local economic growth.

For many parts of the country the emerging devolution landscape looks quite familiar, effectively mirroring previous structures such as Local Enterprise Partnerships (LEPs), so Strategic Authorities will already have a shared agreement on growth priorities and challenges. For others, the economic geography will have changed quite significantly, necessitating a fundamentally different approach that is shaped by newly formed partnerships and their associated evidence base.

Added to this is the need to ensure that special policy areas such as the Oxford-Cambridge growth corridor ("Europe's Silicon Valley"), which cut across new devolution geographies, are supported to achieve their potential as new funding and delivery structures are developed.

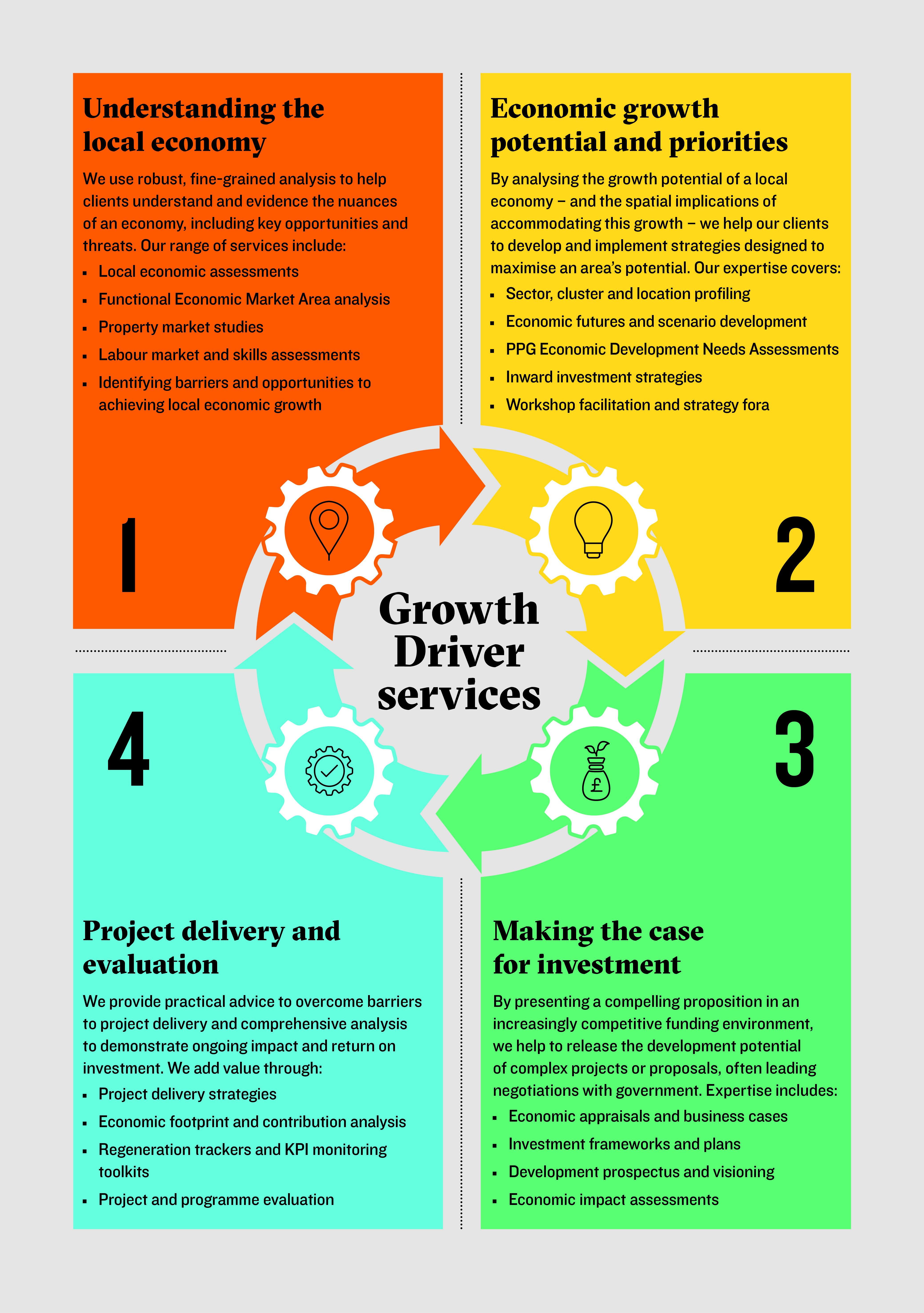

How Lichfields can help

Growth Driver is our package of tools and services designed to help Strategic and Local Authorities realise their potential and maximise their impact on local economies.

This is structured around four key service areas which have been applied successfully within a wide range of locations across the country. Growth Driver is underpinned by Lichfields’ team of experts with national experience of analysing complex economic intelligence and trends to help our clients develop robust and innovative solutions.

Please

get in touch to find out more.

Footnotes

[1] For example by the Leaders of North Warwickshire Borough Council, Nuneaton and Bedworth Borough Council, Stratford-on-Avon District Council and Warwick District Council

[2] Institute for Government - local government unitarisation

[3] Ministry of Housing, Communities and Local Government, English Devolution White Paper, December 2024

[4] For the purposes of our analysis, we have drawn upon Institute for Government’s overview of the current status of devolution in England, as at February 2025

[5] The Industrial Strategy focuses on those sectors which offer the highest growth opportunity for the economy and business. Eight growth-driving sectors have been identified: Advanced Manufacturing, Clean Energy Industries, Creative Industries, Defence, Digital and Technologies, Financial Services, Life Sciences, and Professional and Business Services.

[6] We have used a locational quotient (‘LQ’) approach, a measure of an area’s industrial specialisation relative to a larger region (in this case England). An LQ greater than 1.0 means that the devolved authority area has a higher level of specialisation than is seen across England as a whole.

Image credit: Benjamin Elliott via Unsplash