Winding ourselves back to April 2022, Plan-making was in a perilous state. Planning reform was on the horizon so many emerging Local Plans tackling (or about to tackle) difficult issues – such as Green Belt review, high housing need, or other cross boundary issues – were being shelved, put on ice, or withdrawn.

This led to our blog –

counting the cost of delay – which identified 11 Local Planning Authorities had taken such action. Based on the data available, we then reviewed eight of these authorities and found that c.70,000 homes were caught in these plans which represented a combined construction value of £10.14 billion (using Lichfields

Evaluate): supporting 1,000’s of jobs, generating economic output, and delaying the operational and expenditure impacts that arise from new development.

Nine months on everything has changed but nothing is different.

Where are we today in planning reform?

One of the key reasons for plan delay has been the impending changes to plan-making. The most recent reforms are those now described in the Government’s ongoing consultation on the ‘Levelling-up and Regeneration Bill: reforms to national planning policy’ which runs until 2

nd March 2023. Further details on the proposed amendments can be found in colleagues’ blogs which respectively

summarise the proposals and set out in detail the proposed reforms in relation to

density and character, the

Housing Delivery Test, and

Five Year Housing Land Supply.

These changes were alluded to in a

Written Ministerial Statement (‘WMS’) published by the Secretary of State, Michael Gove, on 6

th December 2022.

‘Summary’

As set out below, a number of Local Authorities have paused plan-making since our last blog with a further flurry since the publication of the WMS, citing the uncertainty caused by this document specifically as the reason for the pause. As we will come on to, since our last blog a further 27 LPAs have stalled, delayed etc (28 including Havant which we originally missed!). Of these, 8 have been since the WMS was published and it is likely that more are on the horizon. Our analysis shows we may be foregoing at least 11,200 homes per annum.

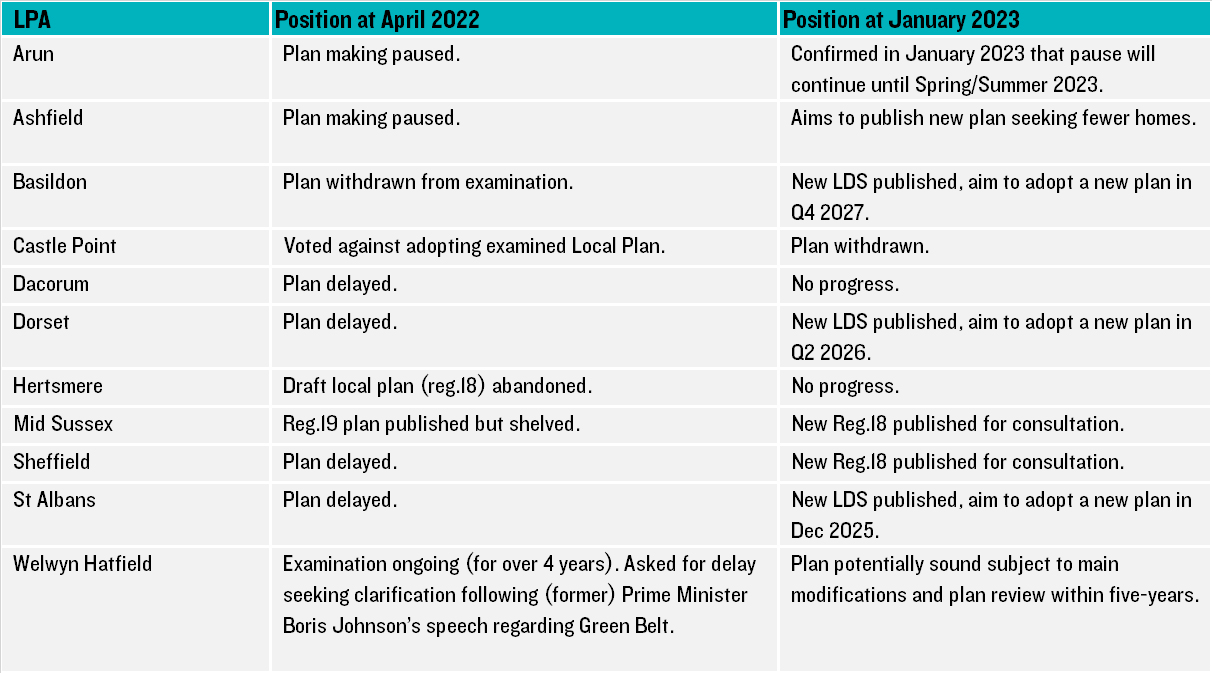

Where are our original 11 LPAs?

Looking back at our original 11 LPAs, what progress has been made? Very little…. It looks like there is some progress in Welwyn Hatfield and Mid Sussex have gone back a step but (albeit with a largely similar plan) are at least consulting. Sheffield have published a new Reg 19 for consultation. The rest either have no progress or at most have published a new LDS.

Following the publication of our previous blog, we were made aware that in addition to our identified LPAs, Havant had also withdrawn their Local Plan from examination in March 2022. This followed concerns raised by the Inspectors regarding the deliverability of housing allocations and how consultation had been undertaken, with Councillors raising concerns regarding ‘unattainable targets’.

Have any more LPAs joined the list?

Unfortunately, but unsurprisingly, yes.

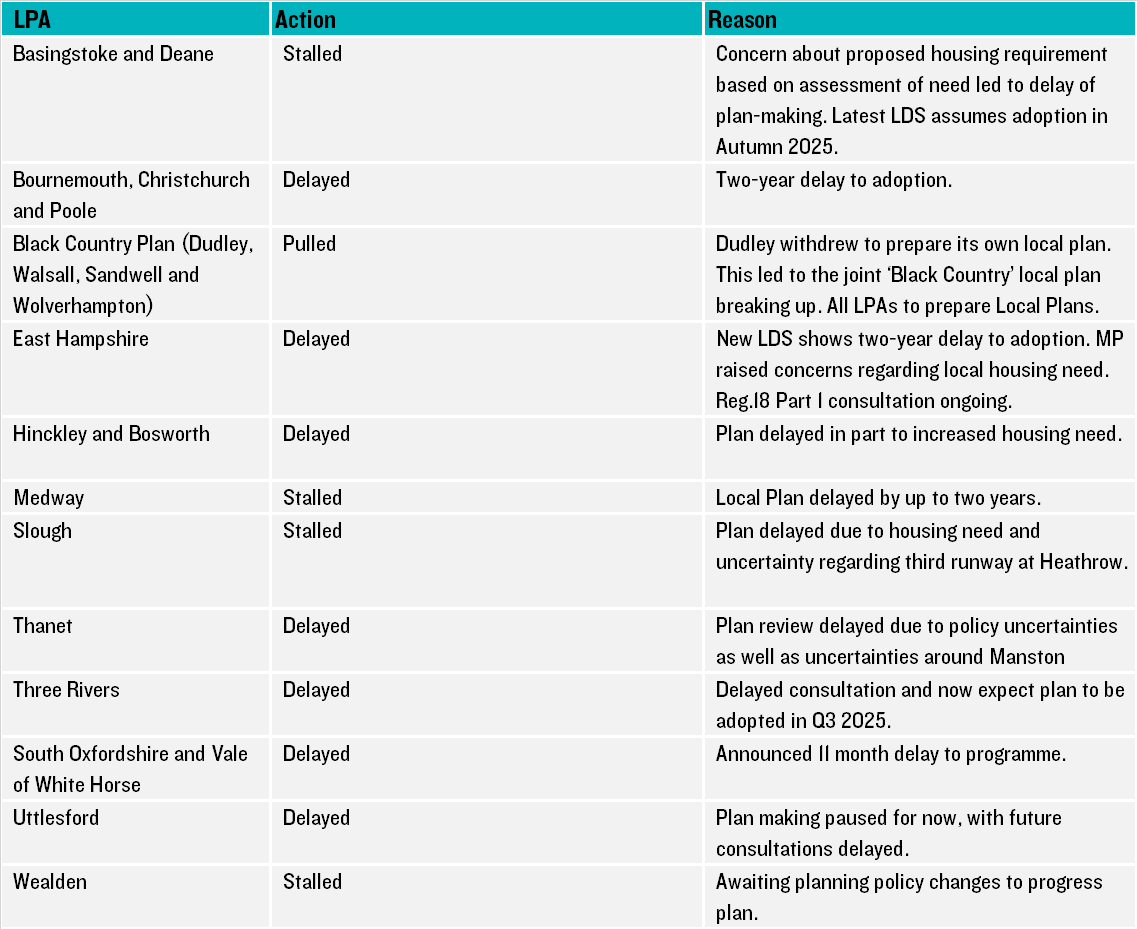

Pre-WMS

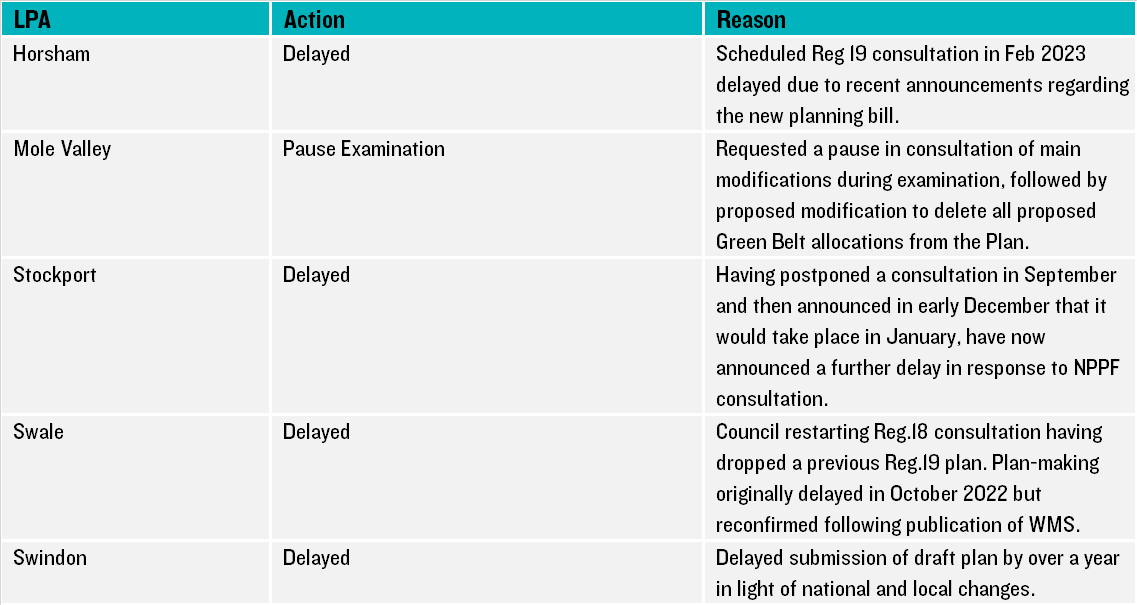

Post WMS, Pre-NPPF Consultation

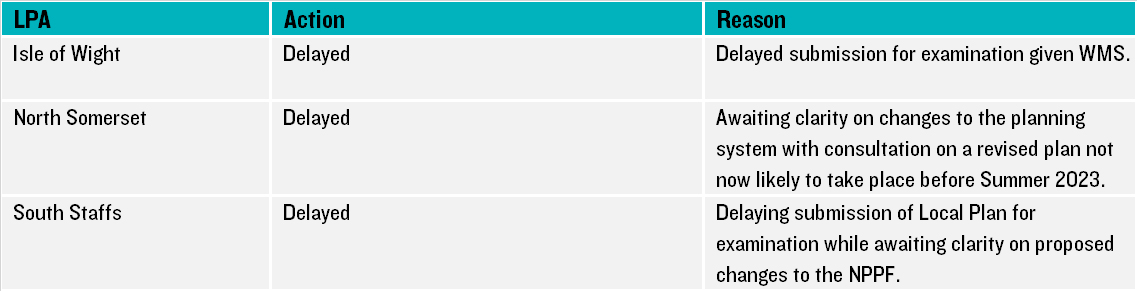

Post NPPF Consultation (to 18th Jan)

There are other LPAs that arguably could be added to the above lists. However, they have either not overtly stated their plan is being delayed, are just slow at plan-making (and not updating LDSs), or are having trouble at examination.

Looking ahead – future delays on the horizon?

Looking to the future, although the NPPF consultation provides an indication of the potential reforms, there is continuing uncertainty which we expect will lead to further Local Plan delays. We have identified at least four LPAs who have hinted at a potential future delay:

-

Teignbridge – while Teignbridge are continuing to consult on their Regulation 19 Local Plan, Councillors agreed to a recommendation which allows the council to review the total number of new homes in the local plan if policy is changed regarding housing targets.

-

Spelthorne – in a statement published on 20 December 2022, the Council set out that the proposed changes to planning policy could have an implication for the number of homes that should be planned for. They have scheduled an extraordinary Environment and Sustainability Committee Meeting on 31st January 2023 to review the changes and their implications for the Plan, and how to proceed with the examination.

-

Gedling – confirmed on 8 December 2022 that a Green Belt site was to be removed from the Local Plan and requested that the government urgently clarify the policy in terms of housing targets.

-

Greater Manchester Spatial Framework – On 18th January 2023, Conservative Councillors in Bury failed to pass their motion to withdraw from the Places for Everyone Greater Manchester Spatial Framework, which could have led to the collapse of the plan. While the Plan survives for now, tensions surrounding it have been widely reported and its collapse would lead to at least 20,340 homes foregone and leave no local authority in Greater Manchester with an up-to-date plan.

Counting the mounting costs

Homes Foregone

Using a slightly different methodology for our ‘homes foregone’ measure, all the 38 LPAs (preparing 33 plans) that have overtly delayed, paused, withdrawn etc their plans combined have an annual housing need of c.38,200 homes

[1]: equivalent to 12.8% of the national figure (outputted by the Standard Method). This compares to an annual delivery of c. 27,000 homes (based on an average of the past three years delivery as detailed in the 2021 Housing Delivery Test).

Were these LPAs to plan for their local housing need (or adopted/emerging figure if higher) in their next plan, then delivery in these areas should eventually rise to the c. 38,200 homes per year requirement. This means we are forgoing c.11,200 homes per year in the absence of ambitious local plans.

Over just a five-year period then, we are foregoing at least c.56,000 homes that might otherwise have been delivered if plans were made and adopted to meet higher levels of need.

This is likely to be a lower estimate. The true figure will be greater because of the gradual build out of legacy allocations which currently maintain supply. In addition, of the 38 LPAs assessed only five have wholly up-to-date plans so the rest are currently relying on ‘speculative’ development to supplement their delivery to varying extents (ironically, this is exactly what the Government’s changes to the NPPF are supposed to prevent). Supply from this source will likely be supressed by the Government’s proposed reforms to five-year supply.

Economic costs

Of the additional 27 LPAs announcing a delay since our last blog (including Havant) only 13 had draft plans published which set out proposed new allocations or submitted plans that we can analyse.

In total, these plans proposed c.74,700 homes on wholly new allocations across their respective plan periods, of which c. 22,600 were meant to be affordable.

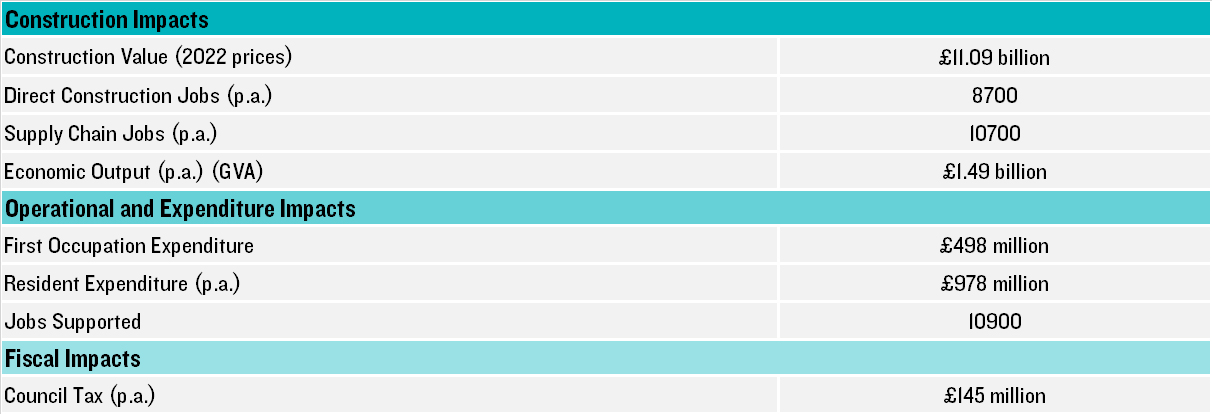

Next, looking at the Evaluate outputs, these 74,700 homes have an estimated combined construction value of £11.09 billion (at 2022 prices, calculated using regional costs). This level of investment would support 8,700 direct jobs, 10,700 indirect jobs with an annual economic output of £1.4 billion (GVA).

Local economies would be hit as the spending growth associated with new development won’t materialise as might have been expected. While not all this spending will be new (i.e. people living in an area moving to a new home in the same area, or money saved for first purchases spent on other goods/services) this expenditure would support 10,800 retail jobs. These developments would also generate £145 million per annum in Council Tax (at today’s rates).

Conclusions

The costs of delay are real. The continuing malaise in plan making locks up growth and the above only shows some of the cost given we haven’t looked at economic development and we aren’t able to review all of the delayed plans. This is obviously not helpful given we may fall into recession, especially when the growth is there to be had. It is more than just the homes and business development though, it’s the new schools, health centres, green spaces, and sports provision that also gets held up. These have significant associated social costs.

As we previously concluded, one could readily recognise the realpolitik drivers of stalling local plans back in April. More than nine months on, the proposed changes in national policy – which appears to be the primary driver for delaying plan-making – seem to deliberately plan for fewer homes. They remain on the horizon but are closing in.

The best way to visualise our current quandary is this

Monty Python sketch. Sir Lancelot – in this case ‘planning reform’ – always appears on the horizon. The question remains, if this has been the impact so far, what will it do when it suddenly arrives at the gates?

[1] This figure is an amalgamated figure of the local housing need (calculated using the standard method) for each LPA or a higher requirement in an adopted or emerging plan (i.e. accounting for unmet needs and growth deals)