Our award winning blog gives a fresh perspective on the latest trends in planning and development.

Fool’s gold? How a rigid approach to affordable housing and benchmark land values for green belt could undermine housing delivery

Matthew Spry20 Sept 2024

The consultation on the draft NPPF has reignited the debate on land value capture through planning insofar as it relates to development that occurs on land that was (or is) designated as Green Belt.

The government proposes that the ‘golden rules’ should apply, which include requiring 50% of homes on site to be affordable[1] and then proposes three options for approaching viability.

First of these is that the Government should “set indicative benchmark land values [BLV] for land released from the Green Belt to inform the policies developed on BLV by LPAs” to be set at a “fair level” allowing for what Annex 4 of the draft NPPF describes as a “reasonable and proportionate premium for the landowner”. The consultation refers to BLVs currently being set at a range of 10-40 times Existing Use Value (EUV) and notes a suggestion it could be reduced to three times EUV. The consultation states it is “particularly interest in the impact of setting BLV at the lower end of this spectrum”

The two other options it sets out (preventing viability negotiation on planning obligations if the price paid has exceeded the nationally-set BLV, and late-stage reviews to secure additional contributions to achieve policy compliance) are to all intent and purposes already part of national policy and guidance[2].

So it is the suggested combination of 50% affordable housing as a standard and a nationally-defined BLV at the lower end of the spectrum that is significant.

The Government’s new policy agenda recognises that release of Green Belt land will be necessary to meet development needs, and in our view, Green Belt land for an extra 75,000-100,000 homes a year could well be needed. In due course, local plans will properly be the vehicle for achieving this (in which landowners and developers will engage with LPA land availability studies) but in the short term[3], the Government’s ambitions for 1.5m homes (or coming anywhere close) largely depends on willing landowners agreeing with developers to invest in promotion of Green Belt land for housing via speculative applications[4] which may or may not be welcomed by the relevant LPA and thus risk incurring the extra costs of a s.78 appeal.

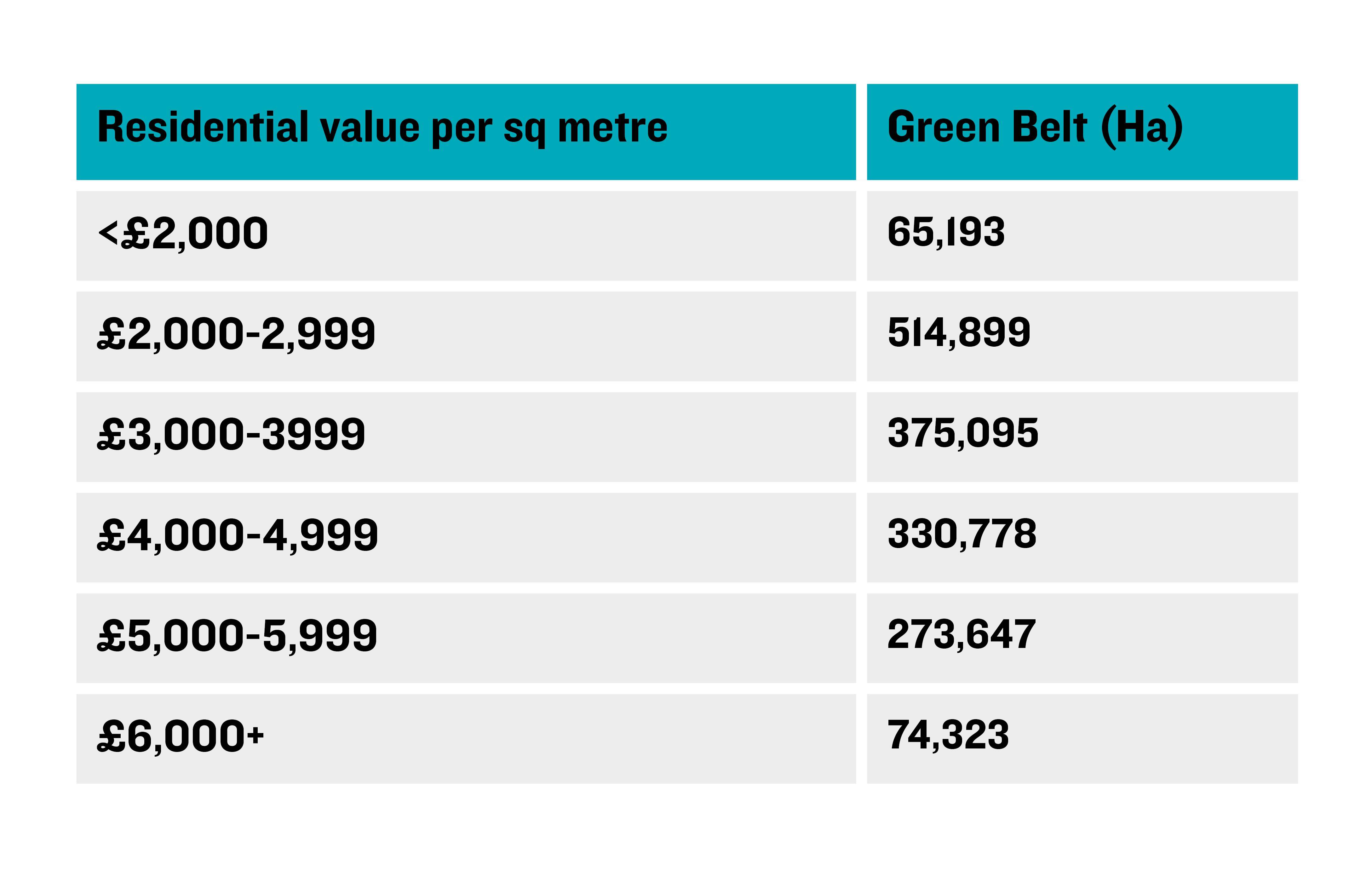

It goes without saying that 50% affordable housing is more than is judged viable in almost all local plans[5], and there are significant differences in values across the country (see Figure 1 below). In general terms, it is unlikely that 50% affordable housing will be viable in areas where residential values are below £4,000 per square metre. These represent 59% of the Green Belt, meaning that this national target will require viability assessment for pretty well any Green Belt development proposal coming forward in those areas (see Table 1). In the 41% of Green Belt where values are above £4,000 per square metre, there may still be other infrastructure obligations which render 50% affordable housing unviable.

Table 1: Area of Green Belt by residential values per square metre

Source: Property Data / Lichfields analysis

Figure 1: Residential values per square metre and the Green Belt

Source: Property Data / Lichfields analysis

So, in stretching affordable housing requirements for Green Belt but also achieving the necessary increase in supply of housing, it is critical that Government calibrates its efforts so that development remains viable, and that landowners, investors and developers are encouraged to bring forward projects for development.

The Government's tentative suggestion to reduce BLVs on a national basis speaks to a view - which appears on a recurring basis in certain policy circles (and seemingly not always fully cognisant of the reforms to viability introduced by the PPG in 2019) - that there remains large amounts of untapped value in the increase in land value arising from permission.

But all that glitters may not be gold. If the real world effect (albeit unintended) is to see less development coming forward, would this proposal represent a planning form of iron pyrite?

What should influence an appropriate BLV?

Much of the debate over the level of BLV is dominated by the question of:

how much premium above EUV is necessary to “reflect the minimum return at which it is considered a reasonable landowner would be willing to sell their land”[7].

That is indeed important, but it is not the only consideration. As noted by Knight Frank[8], also relevant is how the BLV relates to two important steps in the planning and development process, namely:

The uplift necessary to secure the investment in land promotion (converting its EUV to its BLV through the securing of planning permission[9]); and

Funding up-front infrastructure/servicing of plots for housebuilding.

Each of the three factors is considered in turn.

A. Motivating a willing landowner to sell their land

The 2012 Harman Review[10] identified several considerations involved in setting a BLV that would be sufficient to motivate landowners to make their land available for development:

The appropriate premium above current use value should be determined locally. If the value does not reflect local discussions and conditions and cover all relevant costs, including tax and fees, there is an increased risk that land will not be released. The premium should consider the key landowners in the area, as those with longer-term investment horizons may require a higher premium than those more inclined to sell.

Non-urban sites and urban extensions are more complex, as landowners are typically not distressed sellers and may have longer-term perspectives on land disposal, potentially making a once-in-a-lifetime decision over an asset that may have been in the family, trust or institution’s ownership for many generations. Large greenfield sites often demand significantly higher premiums due to the long-term nature of landownership and the significant implications of selling.

For smaller, edge-of-settlement greenfield sites, landowner expectations may be higher than larger greenfield sites (and more in line with urban areas) because landowners will have in mind the prospect of securing a beneficial permission at some point in the future.

The Harman Review assessment goes to what is apparent to anyone who has tried to secure an option or promotion agreement on land for development: owners are generally highly reluctant to dispose of assets they have often owned for a long time, and from which they derive their income and in many cases, their whole way of life.

The review of BLVs by Lichfields cited by the Government’s consultation[11] did identify a range of 10-40 times EUV in various viability studies, but the amounts varied both within and between local areas, and – importantly – between sizes and types of site. In 52% of studies, the BLV for greenfield land sat within a range of 15 to 20 times EUV. For smaller sites, it is common for smaller sites to use an EUV plus a fixed amount of, say, £0.5m per hectare. The expectations of a landowner will also be clearly influenced by their view of how much development land is worth taking into account local property values, including those of alternative uses for which the site might be developed.

The three times EUV reference is drawn from work by Professor Glen Bramley[12] in which he floats the idea of a much-reduced uplift in these terms:

“It may well be that prices at that level [15 times EUV] are needed to persuade long term (and other) landowners to sell, although some of the surprisingly large figure for greenfield land may go into the process of getting sites into or through the planning system. It is clearly way in excess of what a working farmer would need to move to a different farm. I would hope and expect that an incoming Government would change expectations clearly in this respect, certainly for greenfield land, so in my version I have reduced the mark-up from 15 times to 3 times. This may be an area for further discussion, as we do not want the supply of sites to dry up.”

The last point flagged by Professor Bramley is clearly the million dollar (per hectare?) question. The Government’s consultation paper suggests that Green Belt has been subject to “severe restrictions on development” and that this must logically dampen landowner expectations compared to other greenfield land. But in fact, there has been a steady flow of development on land that is or was Green Belt over past decades, either justified by ‘exceptional circumstances’ through local plans or, less commonly, applications via ‘Very Special Circumstances’: MHCLG figures show that since 2013, between 2,000 and 4,000 hectares of Green Belt land have been developed each year[13]. Landowners with sites on urban edges in sustainable locations in areas with high housing need will have in mind that – with national policy that waxes and wanes - there is a reasonable prospect over a period of decades that their land might be developed just as with any other land.

But in any event, as reluctant sellers, it is about landowners receiving an amount that makes this ‘once only’ transaction worthwhile from their perspective.

An element in this respect is the prospect of an alternative use; some sites will be suitable for release for commercial uses, such as logistics or data centres, and if the equivalent 'golden rules' for these other uses draw down less of the development value than the 50% affordable housing equivalent, leaving a higher residual land value, it could make it more likely that landowners on possible residential sites hold out for what they might expect to achieve from that alternative use.

The final factor is of course that the BLV amount needs to reflect that an uplift in land value received by the landowner will be subject to capital gains tax (currently 24%, but more if this were increased, as speculated, to 45%[14]). Ahead of this, there are also promotion/planning costs to be deducted. This takes us to the next element of the BLV.

B. Investment in land promotion

Moving a site from EUV to its BLV typically requires investment in planning: securing an allocation in a Local Plan and an implementable outline permission. This is necessary to establish the principle and broad scale of the site’s residential development potential.

This does not happen automatically, for a host of reasons that include those related to the need for local plans to present a range of options before selecting sites, as we discussed here. And the costs – whilst varying depending on circumstances - can be significant:

Research has found the costs of evidence to support an outline application for SME builders is now estimated at £125,000 plus application fees[15];

Henley Business School at the University of Reading presented a case study of a 2,000 home scheme with promotion costs of £1.5-2m[16];

The North Essex Garden Communities SPV reportedly spent £6.8m to promote its three sites through the Local Plan, of which only one was eventually allocated[17]. This excludes any planning application costs;

The CMA found the direct costs associated with making planning applications can range from around £100,000 per application to around £900,000 per application depending on the size of a site[18]; and

If taken to appeal, the costs of an inquiry can easily reach £200,000-500,000[19].

Knight Frank estimate a cost of £25,000 - £40,000 per gross acre to promote new settlements[20], and in our experience this is comparable with other large sites.

Presently, LPAs rely on the private sector (landowners, housebuilders or specialist promoters) to assist in plan making by putting forward sites for consideration and provide the evidence necessary to satisfy the plan maker (and in due course examining Inspector) that the sites are suitable and meet the relevant NPPF tests. There is limited appetite or capacity in the public sector to promote multiple sites through their own local plans and no plans to nationalise land promotion[21]. Even were there such ambitions, they would be costly and take several years to mobilise.

For planning applications that run ahead of the local plan on unallocated land (i.e. speculatively), it is self-evidently reliant on the landowner or a private sector promoter acting on its behalf to drive that process by investing in the preparation, submission and negotiation of planning permission (with all the risks involved, notably of not succeeding).

Taking the risk on a planning application is critical if the Government is to come close to its 1.5m homes ambition, reversing the shrinkage in the housing pipeline that has emerged in recent years, compounded by the lack of up to date local plans[22].

The University of Reading described the role of land promoters thus:

Specialist land promoters can be viewed as market intermediaries with relatively high appetites for and tolerance of planning risk. In order to operate effectively in the strategic land market, they will also usually have access to the resources and resilience to absorb and manage such risk. For some landowners, land promoters are essentially land venture capitalists. Given the site-specific nature of planning risk, the ability of large land promoters to promote and consequently to diversify across a number of sites, provides a source of competitive advantage.

Having the ‘resources and resilience’ means receiving a sufficient return on their investment which they will secure from what is typically their share that is reported as 10-15% of the proceeds of the land sale. Given the time taken (measured in many years), that large costs are often incurred early in the process, and that not all land promotions will be successful, the promoter (be that a housebuilder, landowner or specialist promoter) will typically require a significant return on investment which Knight Frank report as being five times the costs incurred. The BLV will thus need to be set to provide a sufficient return to achieve this, whilst still leaving sufficient value for the landowner after capital gains tax. Without this, there would be no business case to support the investment in that activity or persuade the landowner to make their land available in the first place.

To this it might be said that in due course a more streamlined planning system and positive policy environment will increase certainty, reduce the costs, and reduce the rate of return required by promoters. However, that is an unproven hypothesis, and its impacts (if successful) are in the medium to long term. In the short term, the Government's housing ambitions require these organisations - and their funders - to invest now to bring forward land.

C. Funding up-front infrastructure/servicing of plots for housebuilding

The third element is that, once the principle of development is established through a planning permission, it is necessary to invest in up-front infrastructure and servicing the land for development. The Knight Frank analysis[24] refers to research on up-front infrastructure on large new settlement schemes of between £40,000 - £63,000 per plot and viability studies for local plans typically refer to costs of £5,000 to £25,000 per plot, with others providing equivalent figures per gross or net hectare. Obviously, on larger sites, the up-front infrastructure can be split into phases, but the amounts will vary significantly. The key challenge is that the works that are required before sufficient income is generated from house sales will need working capital through some form of loan facility where the residual value of the land with permission acts as security collateral, probably at no more than a 60% Loan to Value (LTV). The Knight Frank analysis identifies on its new settlement case study that the initial debt-funding requirement amounted to around one fifth of the total enabling infrastructure cost.

The alternative, of course, is for more significant up-front state funding of infrastructure, but this will in any event be needed on sites with large abnormal costs and there is no sense at all that the state has the resource to front-fund all residential development sites.

Drawing it all together, what does this mean for BLVs that support delivery of new homes?

In simple terms, the value of the land sufficient to support delivery of new homes needs to be the minimum of what is necessary to satisfy the three factors.

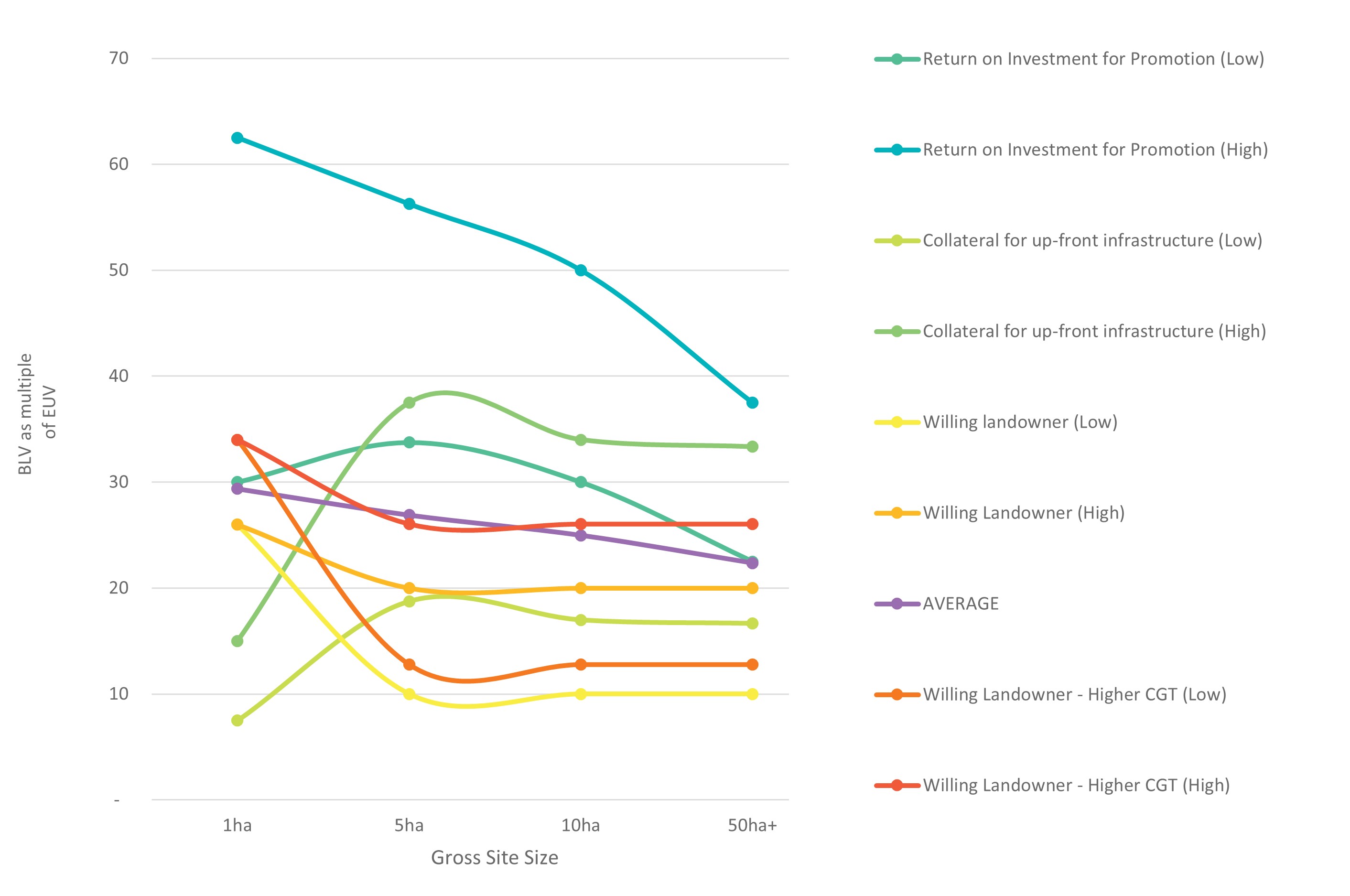

Every site will be different, but setting a BLV for viability purposes in the planning system needs to be resilient to different circumstances, such that sufficient deliverable land is brought forward. To illustrate what this means, in a simple modelling exercise we have identified a range of different BLV estimates based on what factor is seen to drive the land value required:

Identified four notional typologies of sites with gross areas of 1, 5, 10 and 50 hectares;

Derived net developable areas based on typical site ratios ranging from 0.4 (for sites of 50+ha) to 0.9 (for sites of one hectare) to which is applied a density of 40 dw/ha. This reflects that sites need to accommodate landscape/open space/bio-diversity net gain and infrastructure.

Developed two bookend scenarios (high and low) for applying our various assumptions;

Assumed promotion costs per hectare of £75,000 to £100,000 for a site of one hectare, ratcheting down to 60% of those costs per gross hectare as site sizes increase up to 50 hectares, with a rate of return for the promoter of between four and five times that cost. We then identified the necessary BLV to support that return if it were 40% of the total increase in land value achieved (and 50% for the small site of one hectare) albeit in many promotion agreements what is assumed is 10-15% of the uplift (which would necessitate an even higher uplift);

Applied bookends for what a willing landowner would require to motivate them to sell their site to between 10 and 20 times EUV for sites of 5, 10 and 50 hectares, with a EUV+£500,000 for a site of one hectare;

Applied a capital gains tax rate of 24% to the uplift in land value for each of the 'willing landowner' bookends after deducting 15% for the land promotion return to identify the net return to the landowner and then identified what the BLV would need to be for the landowner to achieve the same return if CGT applied at 45%.

Assumed that up-front costs per plot (not total infrastructure costs per plot) to service land of between £2,500 and £5,000 for sites of one hectare increasing in stages to between £10,000 and £20,000 per plot for sites of 50 hectares and identified what the BLV would need to be to secure a loan at 60% LTV.

The outputs from this modelling exercise, which are to illustrate a concept, not to set what should be used for a BLV in any given area, show the BLV as a multiple of EUV (assumed to be £20,000 per hectare in all cases) for each driver of the BLV are shown in Figure 2 below.

Figure 2

In theory, for a site to successfully come forward, one would assume that the BLV would need to be the highest of the three drivers of land value in any reasonable scenario for a site (either what justifies the promotion cost, secures an adequate return for the landowner after CGT to incentivise them releasing their asset, or to fund upfront infrastructure) as otherwise the site/project would not be either promoted, released or funded. In some of our notional scenarios for the smaller site examples, the combination of promotion return and what a willing landowner would require after CGT would suggest these sites would not in fact come forward, which probably goes some way to explain why there is a paucity of smaller sites allocated and coming forward, and why streamlining and de-risking planning for small sites is so important, particularly for SMEs.

The cost and value factors shaping the different elements of this calculation will clearly vary between sites, but setting a BLV to inform planning policy needs to account for a representative mix of sites on which an area will sensibly rely to meet its housing needs. In this regard, our analysis of typologies shows that the different factors will typically suggest BLVs at least to the middle or upper end of the 10-40 times EUV range identified earlier and nothing remotely supports the idea of setting BLV at the lower end, let alone at just three times EUV. Even before considering landowner expectations, promotion costs are a very high proportion of the total costs for small sites, whilst up-front infrastructure can require significant collateral for larger sites. A crude average across our different drivers and the low and high bookends equates to a BLV of between 23 and 30, but it is obvious that circumstances could accumulate on a site to require a higher level.

Summary and conclusions

Drawing from the preceding analysis, the following conclusions emerge:

It is unlikely that 50% affordable housing will be viable in most Green Belt LPAs under the current approach to viability. Although some locations - such as those with residential values of £4,000 or more per square metre (equivalent to 41% of the Green Belt) – might see 50% as being achievable on some sites, this will be the exception (particularly outside the South East – see Figure 1) and explains why the majority of LPAs even in the most prosperous markets set affordable housing requirements in local plans at no more than 40%. Although having an affordable housing premium for Green Belt is politically understandable, setting a flat national target at 50% is likely to mean viability testing is required on the majority of Green Belt and Grey Belt sites that might come forward, adding cost and uncertainty, especially for any applications or allocations that were made under existing (to be previous) NPPF policy.

Given the above, applying the proposed new approach immediately on adoption of the new NPPF would catch a number of live sites/applications where landowners, promoters and housebuilders agreed commercial terms in good faith based on current Local Plan affordable housing targets, and undermine their ability to come forward.

It would appear imprudent to set a national BLV for Green Belt sites, especially at the lower end of the 10-40 times EUV range, given the multiplicity of different factors influencing this value across different locations. Setting it nationally at a high level might mean it over-estimates the BLV in some places and sees less value capture. The Harman Review made clear that BLV was influenced by local factors, and this is reflected in the current PPG guidance on how LPAs should determine viability for their local plans, setting BLV locally in consultation with landowners, developers and other stakeholders.

There is no evidence to support the idea that reducing BLVs for Green Belt land below what would result from the approach generated by current PPG guidance to other comparable local land would be consistent with delivery. As it stands, in many areas it would not be willingly made available by landowners, be promoted, or produce fundable schemes at any scale if a lower BLVs are imposed for these reasons:

a) Landowners are often reluctant sellers and take a long-term view which informs the value they demand. They will have in mind what their land is worth, taking into account that although Green Belt is a restrictive policy, there has been a persistent flow of Green Belt land developed over past decades. In most cases, they will have to pay capital gains tax at 24% on any net receipts they receive after promotion costs are deducted, and there is speculation this may increase to 45%. Set the BLV too low and it will simply not be worthwhile for many owners causing a ‘land strike’.

b) Land promotion is a necessary part of the planning system and it relies on the private sector investing in the lengthy and expensive process, spreading the risk across a portfolio of sites, reflecting that an implementable permission may or may not transpire, dependent on whether i) land is allocated in a plan (which may or may not be produced) and/or ii) a costly application is approved or refused by LPA. Taking into account the costs and risk, it is easy to see how land values may need to absorb costs of £100,000 or more per ha before the landowner’s return and require BLVs that are 40 times EUV. An examination of why land promotion activity requires the rate of return it does, needs to look beyond simple planning approval rates at application or appeal, and consider the time it takes, and the extent to which much promotion activity does not even make it to the application stage.

c) Developments require up-front funding at anything between £2,500 to £20,000 per dwelling (depending on the site, its size, location, abnormals etc) to deliver infrastructure that services plots for building homes. The land value is often used as collateral to support loans at a 60% LTV to unlock the sites before income from house sales is forthcoming. Our modelling suggests this factor alone requires a BLV of up to 38 times EUV on sites of 5ha or more.

Although there is a theoretical role for the public sector to acquire sites – including through CPO – and then fund up-front infrastructure, this is not a feasible solution for bringing Green Belt land forward at necessary scale or timeframes, because:

a) The Government’s goal of 1.5m homes by July 2029 is fundamentally dependent on sites being promoted ahead of local plans, often in areas where LPAs are at best ambivalent (and often hostile) to Green Belt development in the first place;

b) It is simply inconceivable that the 180 LPAs with Green Belt across England or Homes England will – in the next five years – have either the resources or inclination to speculatively invest in acquiring multiple sites at EUV and then preparing and submitting multiple applications at any scale, particularly in areas where local residents are hostile to the idea of Green Belt development;

c) Even through the local plan process - which might be relied upon for sites that deliver in the next parliament - the legal and policy obligations on plan makers rely on scores of alternative site options being available to support the testing of reasonable alternatives and for evidence to be available that demonstrates the ultimate deliverability of prospective allocations. This promotion activity – with all its costs – applies to every local plan cycle.

d) There is not sufficient funding resources or administrative bandwidth – currently identified – for Government (itself, via Homes England, or through LPAs) to up-front fund (or under-write) infrastructure investment at the scale required to bring forward new homes on multiple sites in every LPA.

This is not to diminish the prospect of the public sector unlocking specific large-scale new communities or unblocking stalled sites of strategic significance - through funding, CPO or good old-fashioned bashing together of heads - and this will have an important role. But the idea the state would in the future become the predominant promoter and deliverer of residential land is simply not plausible even were it considered desirable.

Recommendation

Based on the above, it is recommended that:

Any Green Belt site should apply the same affordable housing policy requirement as the existing/emerging Local Plan requirement that would apply on any greenfield site as there is no real-world difference between the sites that would impact on its viability.

If an affordable housing premium for Green Belt is to be maintained (and the political rational is understandable), this should be set in national policy at a level linked to the existing local percentage requirement from the most recent Local Plan, for example at five or ten percentage points above.

Viability assessments, where necessary, should be carried out based on the current approach to viability in the existing PPG including locally-set BLVs.

To ensure the new policy does not disrupt the flow of existing Green Belt sites, a transition arrangement should apply to exempt from any new ‘golden rules’:

a) current planning applications submitted within a month of the publication of the new NPPF to allow for schemes that are currently submitted or were formulated (and commercial agreements formed) pursuant to existing national policy proceed; and

b) applications submitted at any point on land that was allocated for development having been removed from the Green Belt in a local plan prepared pursuant to the existing NPPF.

Footnotes

[1] The other ‘Golden Rules’ identified in b) and c) of para 55 of the proposed Framework requiring “necessary improvements to local or national infrastructure and the provision of new, or improvements to existing green spaces” are unlikely to represent a significant change from what would be necessary in any event.

[2] The Planning Practice Guidance on viability already states “ The price paid for land is not a relevant justification for failing to accord with relevant policies in the plan” and “under no circumstances will the price paid for land be a relevant justification for failing to accord with relevant policies in the plan.”. See at ID: 10-002-20190509 and ID: 10-006-20190509. Late stage reviews are already part of the planning firmament, see PPG ID: 10-009-20190509 and of course in London (they are not without complications, not least in terms of extending the time it takes to agree s.106 agreements).

[3]Due to the absence of Local Plans that provide for anything close to the higher levels of local housing need.

[4] This is explicitly recognised by the proposed changes to the NPPF at para 152 with triggers for the development of ‘Grey Belt’ land.

[5] In St Albans – which has some of the highest house prices outside London – the evidence-based requirement is 40%.

[6] Prepared pursuant to an instruction from the Home Builders Federation (HBF) and the Land, Planning and Development Federation (LPDF)

[14] See this piece in the Times (£) which says “Capital gains tax (CGT) is paid on the profits made from the sale of property (other than your main home), businesses, shares and most possessions worth more than £6,000. Basic-rate taxpayers pay 10 per cent CGT on most gains, but 18 per cent on property. Higher and additional-rate taxpayers pay 20 per cent CGT but 24 per cent on property gains. There is widespread speculation that Reeves could increase the rates so that they match up with income tax, which would mean 45 per cent for additional-rate payers.”

[15] Lichfields, Small builders, big burdens, September 2023 available here

[16] See this analysis by Henley Business School at Reading University

[18] See para 4.30 of the CMA Housebuilding Study Final Report here. These costs exclude internal staffing costs and the work ahead of a planning application, including promotion through the Local Plan process. We assume they also exclude appeal costs.

[19] Whilst an appellant can sometimes seek and secure an award of costs where an Inspector judges the LPA’s behaviour unreasonable, this is rare.

[20] See Knight Frank analysis here. It has been a valuable source of information for the analysis in this paper.

[21] Homes England’s role is to support release of housing land in a more targeted way and/or through strategic partnerships, not to oversee the promotion of all potential housing land.

[22] See analysis here of the challenge facing the Government in achieving 1.5m homes in this parliament.

[23] A figure validated by Lichfields discussions with specialist land promoters.

[25] Current pressures in the Registered Provider sector are likely to make this more rather than less challenging

[26] The three-times EUV referenced in the Bramley paper is not a remotely credible proposition for greenfield land.

[27] As a broad indication of the scale of the challenge, one might reasonably assume that land sufficient for 75,000+ homes is needed on Green Belt land each year, equivalent to perhaps 1,000-1,500 individual active developments each year (delivering 50-75dw per year), which across 180 LPAs with Green Belt land means the equivalent of perhaps 5 – 8 projects in each LPA every year. Given the ambivalence of many planning committees to Green Belt sites, this would require more than 5 - 8 applications being submitted every year as some might be refused. The total up front cost of promotion would be significant.