From 28 June 2021, and subject to transitional arrangements, English national planning policy will include a home meeting the criteria of a First Home within the definition of ‘affordable housing’.

On 24 May a Written Ministerial Statement (WMS) was made setting out the policy, including the First Homes criteria and transitional arrangements, with further details in planning practice guidance published on the same day.

The same WMS also explains the replacement of the entry level exception sites policy with a ‘First Homes exception site policy and a new model for shared ownership. This blog focuses on what First Homes are, the new policy requirement and when First Homes will be introduced (they already have been). A blog by my colleagues looks at the policy and its potential impacts in more detail:

First Homes – dicing with the discount.

National policy on First Homes

From 28 June 2021, in England, national policy will say that at least 25% of all homes delivered through developer contributions should be sold as First Homes.

What is a First Home?

A First Home is:

- discounted in perpetuity by a minimum of 30% against the market value with plan-makers able to set 40% or 50% in perpetuity discounts where need is evidenced, and developers permitted to offer higher in perpetuity discounts

- after the discount has been applied, the first sale price of the home (my emphasis) must be no higher than £420,000 in Greater London or £250,000 elsewhere in England with plan-makers able to set lower price caps

- sold with a mortgage or home purchase plan for at least 50% of the discounted purchase value to a person meeting the First Homes eligibility criteria

- a primary residence, not used for investment or commercial gain, albeit it may be let for up to two years

- secured by a s106 agreement to ensure its delivery and the necessary restrictions on title[1] (a model s106 agreement for First Homes is being devised)

Who is eligible?

First Homes are to be “prioritised” for first time buyers (as defined in legislation already for the purpose of stamp duty relief). The local authority may set local eligibility criteria. The policy provides examples of criteria that might be applied, such as key workers, local connection, different income caps, but this is not an exhaustive list. Members of the Armed Forces and (subject to certain criteria) their partners and veterans would be exempt from a local connection test. So, if no local tests are set, the purchaser must be a first-time buyer purchasing borrowing at least 50% of the discounted purchase value. The purchaser (or purchasers) should not have a combined annual household income greater than £80,000 (or £90,000 in Greater London) in the tax year immediately preceding the year of purchase.

What if there is no demand for a First Home?

The planning practice guidance says that a s106 agreement may include provisions permitting open market sale of a First Home if it is marketed as a First Home for at least 6 months in total and “all reasonable steps have been taken to sell the property (including, where appropriate, reducing the asking price)”.

Where these provisions are included, the s106 agreement must require the seller to compensate the local authority for the loss of the First Home in the way set out in the planning practice guidance.

What is the policy requirement and how does it relate to existing tenure mix policies?

At least 25% of all affordable housing units secured through developer contributions should be First Homes. As with other affordable housing, the policy expectation is that this is provided on-site unless an alternative financial contribution or off-site provision is justified. A quarter of any financial contributions for affordable housing should be used to provide First Homes.

Having “secured the 25% requirement”, local authorities should prioritise social rent, in accordance with local policy and “where other affordable housing units can be secured, these tenure-types should be secured in the relative proportions set out in the development plan”.

Examples of the application of this approach are given in planning practice guidance:

“For example, if a local plan policy requires an affordable housing mix of 20% shared ownership units, 40% affordable rent units and 40% social rent units, a planning application compliant with national policy would deliver an affordable housing tenure mix of 25% First Homes and 40% social rent. The remainder (35%) would be split in line with the ratio set out in the local plan policy, which is 40% affordable rent to 20% shared ownership, or 2:1. 35% split in this way results in 12% shared ownership; and 23% affordable rent”.

(Paragraph: 015 Reference ID: 70-015-20210524)

The proposed development should also meet up-to-date policy requirements regarding cash in lieu contributions.

The local planning authority (LPA) is responsible for calculating the value of the elements of the new affordable housing mix to establish whether a planning application is policy compliant, because it seeks to capture the same amount of value as would be captured under the local authority’s up-to-date published policy.

Where the transitional arrangements do not apply, the LPA is responsible for making clear how existing policies should be interpreted in the light of First Homes requirements “using the most appropriate tool available to them”.

Regarding the application of First Homes policy locally, consideration of the impact of First Homes policy on existing local policies and the “tools available” to the LPA, the planning practice guidance says:

“Local planning authorities are also encouraged to make the development requirements for First Homes clear for their area. The most appropriate method or tool to do this will depend on individual circumstances for each local planning authority. These might include (but may not be limited to): publication of an interim policy statement, or updating relevant local plan policies. Local planning authorities should assess their own circumstances when considering the most appropriate way to achieve this in their context” (Paragraph: 009 Reference ID: 70-009-20210524).

Will the First Homes policy requirement supersede development plan policy?

Not necessarily.

The development plan remains the starting point for the determination of planning applications.

The First Homes policy will be a material consideration – indeed it already is, together with proposals for other forms of affordable housing defined in the National Planning Policy Framework, notwithstanding the transitional arrangements.

A reminder of the difficulties that arise when Government introduces a swift change to national policy on affordable housing provision is the judgment in

Secretary of State for Communities and Local Government (SoS) v (1) West Berkshire District Council (2) Reading Borough Council (2016) (our overview is

here).

In that case the SoS appealed against the Councils’

successful challenge (in 2015) of

national policy introduced in 2014 for a ‘vacant building credit’ and which outlined the circumstances in which contributions for affordable housing and tariff-style planning obligations should not be sought from small scale and self-build development. The judgement led, effectively, to both sides claiming a victory: the Government won the case, but the case makes it clear that there is no ‘blanket approach’ to the application of government policy to decision-taking, or plan-making.

Hence the Government expecting local planning authorities to use the most appropriate method available to them to set out how the First Homes requirements impact on their current affordable housing tenure mix policies and affect the interpretation of policies (see above).

What are the transitional arrangements?

The requirements will not apply to:

- local plans and neighbourhood plans submitted for Examination before 28 June 2021, or that have reached publication stage by 28 June 2021, as long as they are submitted for Examination before 28 December 2021 (and subsequently not to planning applications submitted in areas to which they relate); or

- sites with full or outline planning permissions already in place or determined (or where a right to appeal against non-determination has arisen) before 28 December 2021 (or 28 March 2022 if there has been significant pre-application engagement).

However, the Government says “local authorities should allow developers to introduce First Homes to the tenure mix if they wish to do so”. “They” could mean developers or local authorities.

The transitional arrangements for plan-making are therefore more of a line in the sand than those for decision-making, given the above statement and that the First Homes product is a form of discount market sale housing in any event.

The written ministerial statement notes “The Government will continue to monitor the effectiveness of these transitional arrangements in light of emerging economic circumstances”.

Does this mean that planning applications to be determined prior to the end of the transitional period cannot include First Homes?

No.

Discount market sales housing is already a form of affordable housing, defined in the glossary to the National Planning Policy Framework. According to that definition of discount market housing:

“Eligibility is determined with regard to local incomes and local house prices. Provisions should be in place to ensure housing remains at a discount for future eligible households”.

There are already developments with planning permission that will provide First Homes affordable housing. For example, the

Dylon 2 scheme at Lower Sydenham, granted on appeal on Metropolitan Open Land, which will provide 49 First Homes. The Inspector said:

“Although not policy compliant in accordance with BLP Policy 2 [provision of affordable housing], the provision of 49 affordable units would make a significant contribution to meeting the considerable need for AH in the Borough. I attach substantial weight to this social benefit of the proposal”.

The Government’s

Equality Impact Assessment for the First Homes policy says First Homes will be a reform of the discounted homes programme and acknowledges:

The National Planning Policy Framework already allows local plans to include ‘discounted market sales housing’ that is sold with a discount of at least 20% over market prices. […] delivery remains relatively small scale and we want to substantially increase the build-out of these homes.

What about 'low cost homes for sale' that are not First Homes?

Sub-category d within the definition of affordable housing in the National Planning Policy Framework is “Other affordable routes to home ownership”. This includes shared ownership and “other low cost homes for sale (at a price equivalent to at least 20% below local market value)”. This definition does not refer to the eligibility criteria or discount for owners of the home. The scope to provide low cost market homes for sale that are not First Homes as a form of affordable housing will be squeezed by the policy requirement to provide First Homes. Shared ownership products will also be squeezed in the future, but in the short term up-to-date tenure mix policies may encourage them.

Community Infrastructure Levy relief is already available

First Homes are a form of affordable housing. Mandatory social housing relief from the Community Infrastructure Levy has been available for certain discount market home products since November 2020.

To be eligible for mandatory social housing relief in this category, a planning obligation must be entered into prior to the first sale of the dwelling designed to ensure that any subsequent sale of the dwelling is for no more than 70% of its market value.

The existence of mandatory social housing relief for this form of affordable housing further demonstrates that First Homes can already be brought forward now. However, mandatory social housing relief from the Community Infrastructure Levy is not available for affordable housing products offering a discount of less than 30%.

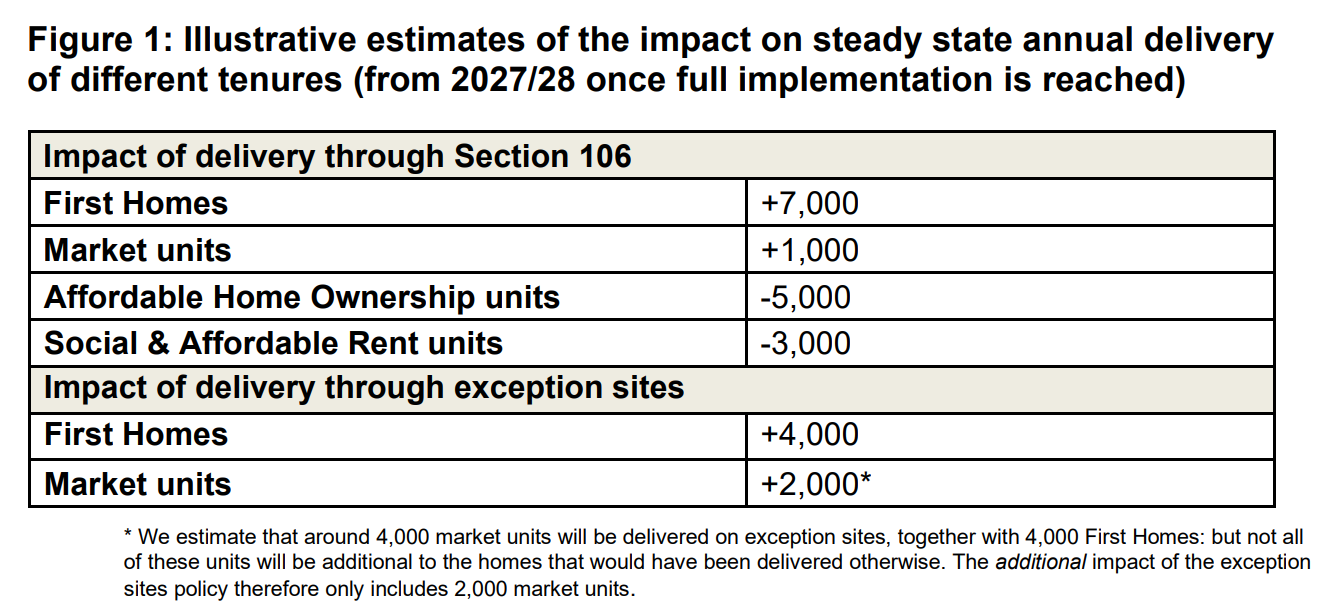

Six years to reach delivery of 7,000 First Homes a year

In October 2020, MHCLG Permanent Secretary Jeremy Pocklington said to the Public Accounts Committee’s inquiry into Starter Homes that implementation of the First Homes policy will not be quick and referred to the transitional arrangements:

“We will need to adjust the planning policy in order to fully implement the First Homes proposal. After that stage, authorities, as they change their policies and update their local plans, will be required to provide First Homes. We are not setting a timetable on that. We are going to learn from the 1,500 homes. This is a policy that will grow over several years. It is not a quick policy to implement”.

This acknowledgement of the time it will take to introduce First Homes policy into development plans is reflected in Figure 1 of the Equalities Impact Assessment for First Homes, which says full implementation will be in 2027/2028:

Summary… and a blog on potential unintended consequences

Low cost homes for sale are not a new form of affordable housing, but the specific criteria and requirements of First Homes are new. Having said that, there are already examples of planning permissions that include First Homes as a type of affordable housing; the Government’s policy intentions have been clear for some time and the introduction of mandatory CIL relief for First Homes or similar products has been around since last year.

Therefore, while the First Homes policy requirement will take some time to filter through to development plans, where developers seek to include First Homes as an affordable housing contribution, there is scope to make the case for this immediately, rather than waiting for the transitional period to end.

A blog by my colleagues ‘First Homes – dicing with the discount’ looks at some potential inherent tensions within the First Homes policy and considers whether the one-size-fits-all approach might have unintended consequences.

[1] Paragraph 006 of the First Homes Planning Practice Guidance says: When a First Home is sold by the developer to the first owner, a restriction is to be entered onto the title register identifying the unit as a First Home. This restriction should ensure that the title cannot be transferred to another owner unless the relevant local authority certifies to HM Land Registry that the First Homes criteria and eligibility criteria have been met, including the discounted sale price.